pxhidalgo/iStock via Getty Images

Since late October, the S&P 500 (SPY) is up roughly 25% despite little change in the earnings of the underlying businesses. Investors can’t get enough of any company claiming to profit from AI or weight loss drugs. Consumer staples stocks/retailers that have discovered the “holy grail” of shrinkflation also have been bid by traders up with some shocking valuations for slow-growth staples stocks and retailers. If the S&P 500 hits ~6000 in the course of this rally, we’ll match the peak valuation of the 1990s dot-com bubble. And if enough retail investors go all in with call options and/or borrowed money, we just might get there. But the stock market mania belies the gradual weakening of the underlying U.S. and global economy. The most anticipated recession in U.S. history is still coming. In the meantime, the soaring stock market is likely fueling inflation, with the Fed now forced to reckon with a pair of hot inflation prints ahead of this week’s FOMC meeting. Recent data shows about half the country is in recession while a speculative bubble is gripping Wall Street. This puts Jerome Powell and the Fed in a terrible spot.

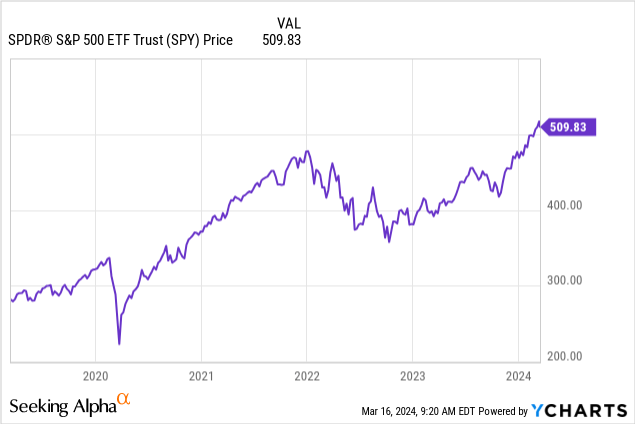

Markets Have Gone Straight Up Since October

The current rally in stocks has gone faster and further than the post-vaccine rally in November 2020.

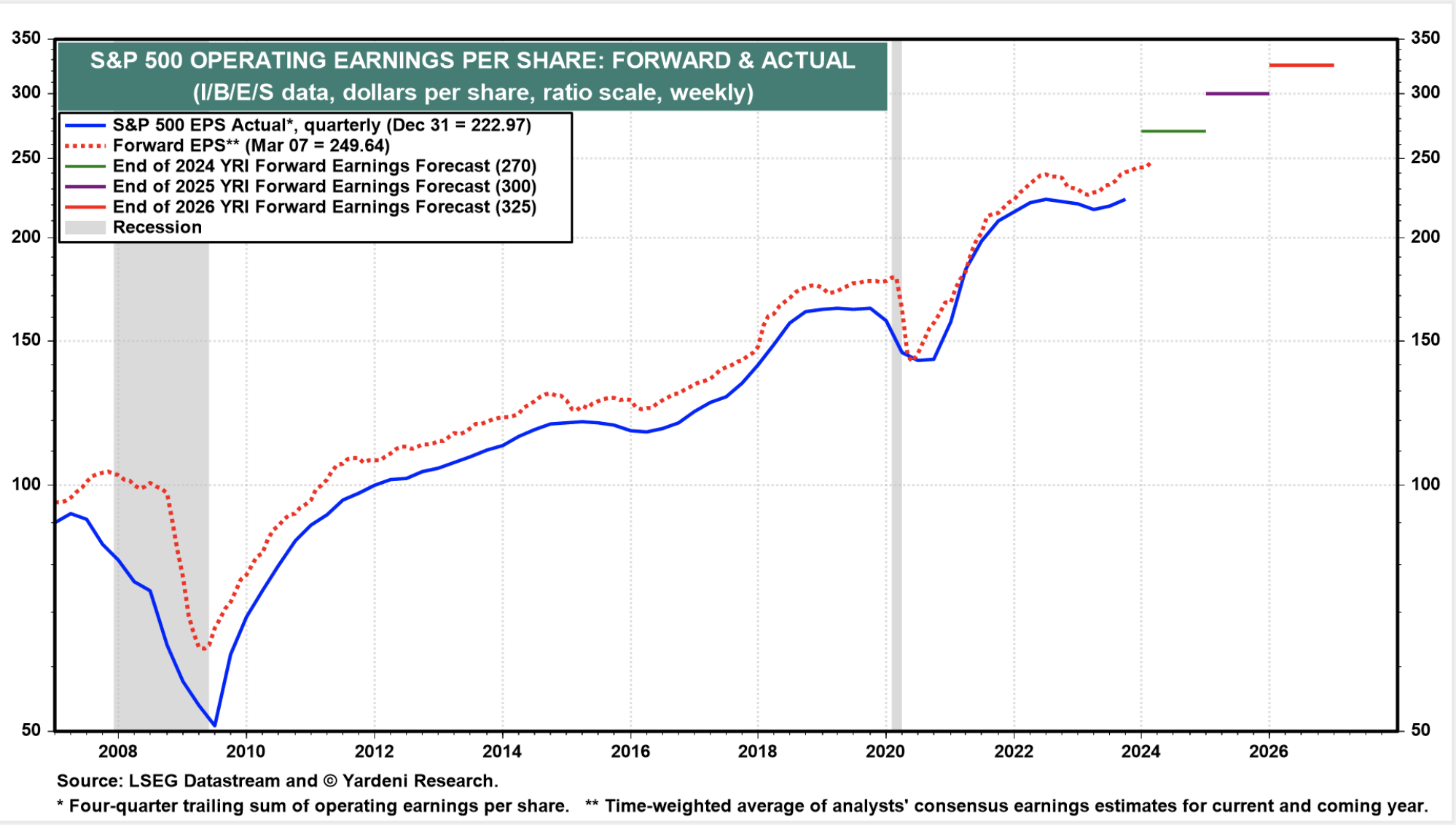

Earnings Are Roughly Flat

S&P 500 Operating Earnings History (Yardeni Research)

Data from Yardeni Research shows that corporate profits haven’t budged much since 2022. Revenues are up, but margins are down, one key reason that margins are down is that pretty much any debt that’s going to be refinanced now is going to have a higher interest rate than it carried before. Profit margins have stopped falling for now, but there has been no sign of an AI-driven boom in margins.

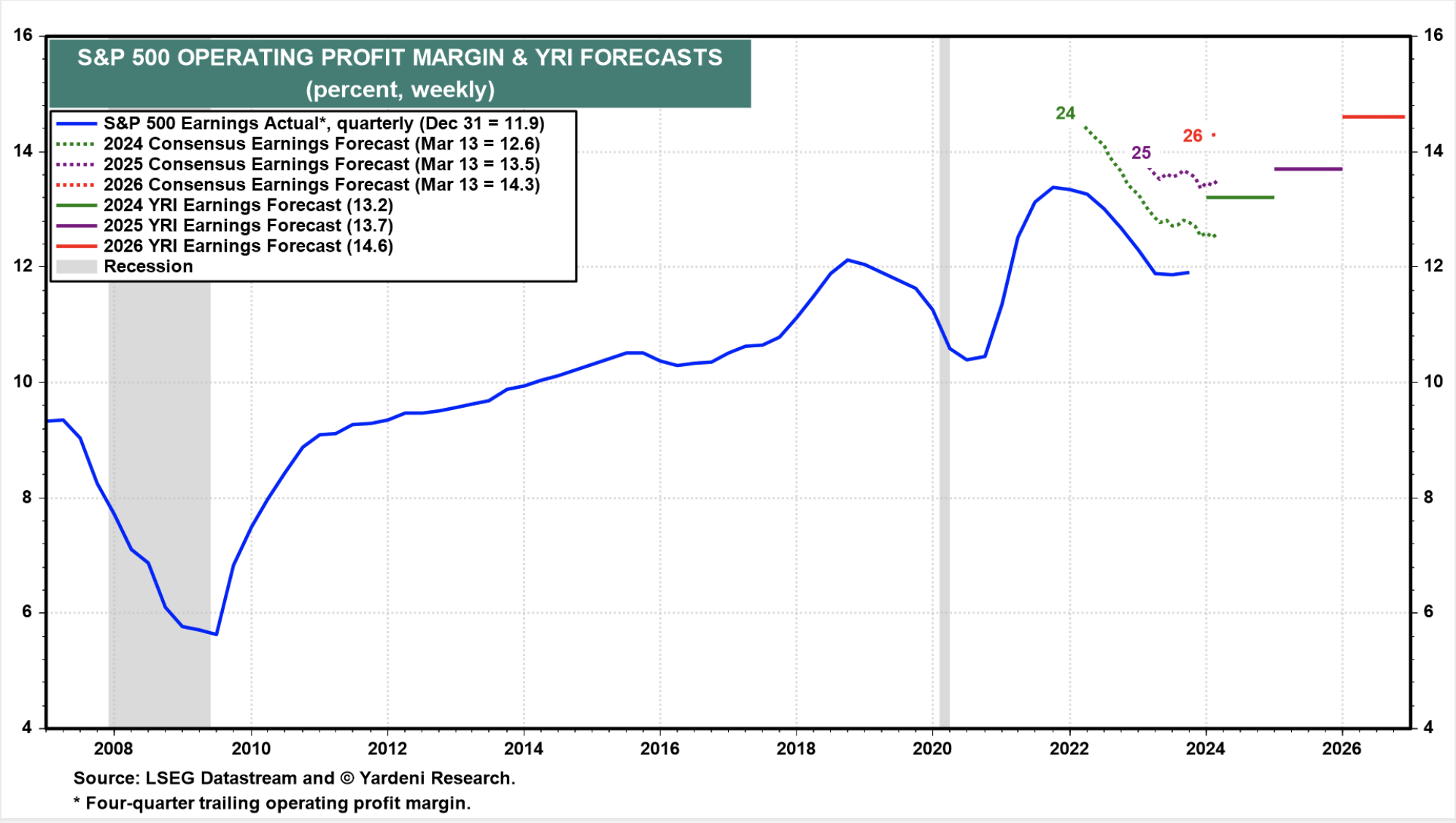

Profit Margins Are Falling From COVID Highs

S&P 500 Profit Margins (Yardeni Research)

This is all kind of weird. 74 companies have issued negative guidance for earnings in Q1 so far, which is far above average. 32 companies have issued positive guidance, which is below average. The data continues to tell us that we’re not experiencing an earnings boom. Ordinarily, for stocks to be worth more you’d want the underlying businesses to be making more money. But the stock market doesn’t seem to care. Investors have been willing to pay ever higher multiples for the same dollar of earnings, with nearly 100% of the move since October simply being from multiple expansion. Sure, crazier bubbles have happened over the past few centuries. However, pundits comparing this market’s slightly lower valuation to the dot-com bubble peak and concluding that this isn’t a bubble are wearing blinders.

The S&P 500 earned roughly $223 in 2023 and trades for above 5100 as of my writing this– that’s good for about 23x earnings. The 21st Century average for stocks is around ~17.5x earnings – this includes the dot-com era, the 2000s cyclical bull market, the brutal bear market of 2008, and the recovery in the 2010s. I can’t think of a durably good reason for stocks to trade for 30% higher valuations than they did when interest rates were 0%.

To this point, AI hype isn’t translating to higher earnings. While the market avoided an outright decline in earnings year-over-year thanks to stronger-than-expected tech earnings, the numbers weren’t all that impressive. If anything, the parallel may be closer to Y2K, when companies and governments spent about $300-500 billion out of fear of Armageddon. In the end, the Internet did deliver on its promise of gradually higher economic productivity, while companies that raised money for 100x earnings or more did not. The fear-driven spending cycle soon ended, leaving the useful innovations to stand and the BS to fade away, along with a glut of Silicon Valley office space and discounted office furniture. The Nasdaq (QQQ) ended up falling about 80% from peak to trough in that cycle.

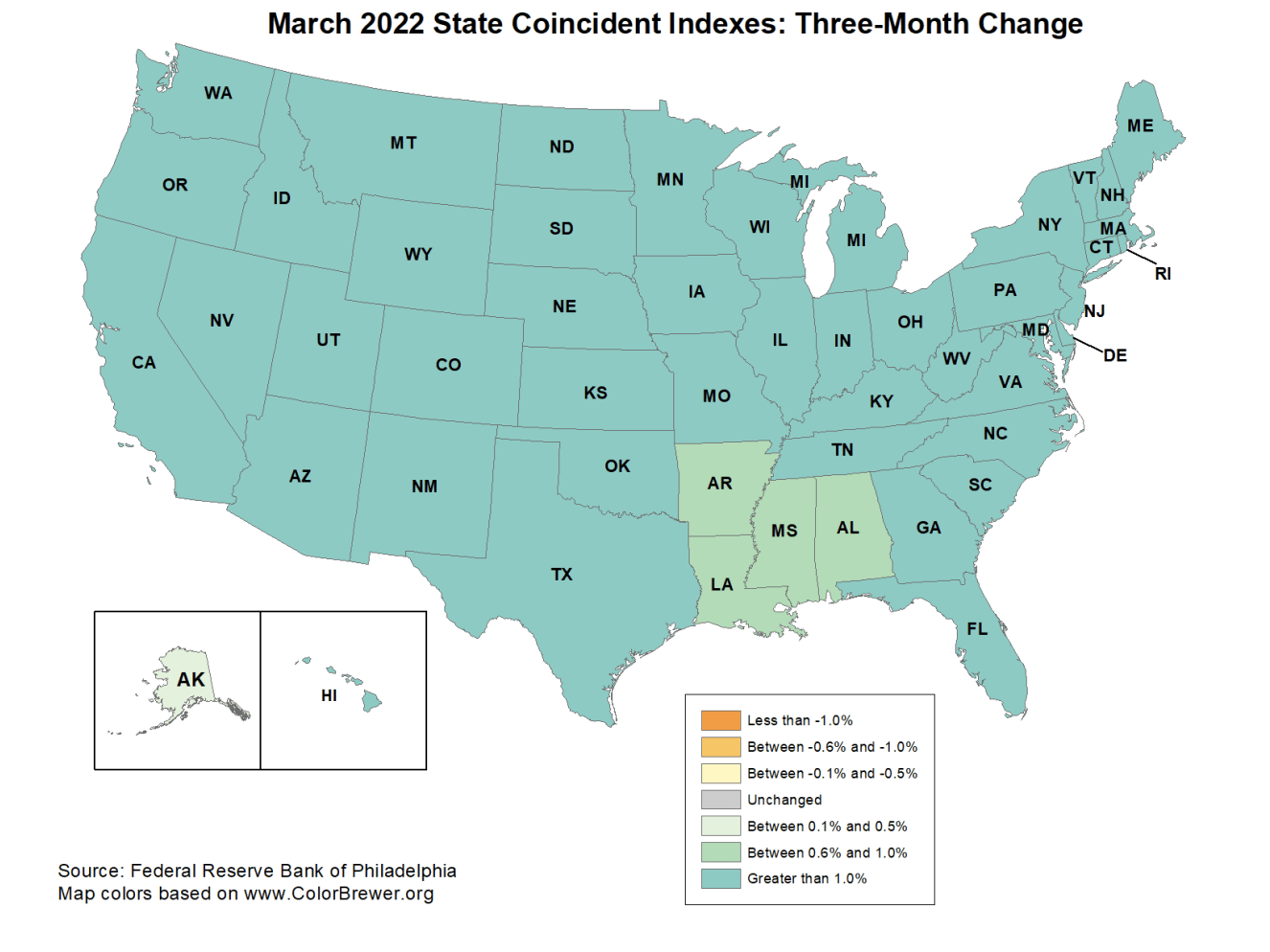

About Half The U.S. Is In Recession

The recession is still coming. We can see it in the state-level economic data from the Philly Fed, and the Fed saw it before we did – that’s almost certainly why they paused hiking interest rates, not because they want retail traders to get rich trading call options on Nvidia (NVDA).

See for yourself:

This was the economy in March 2022, when the Fed started hiking.

March 2022 State Level Econ Data (Philadelphia Fed)

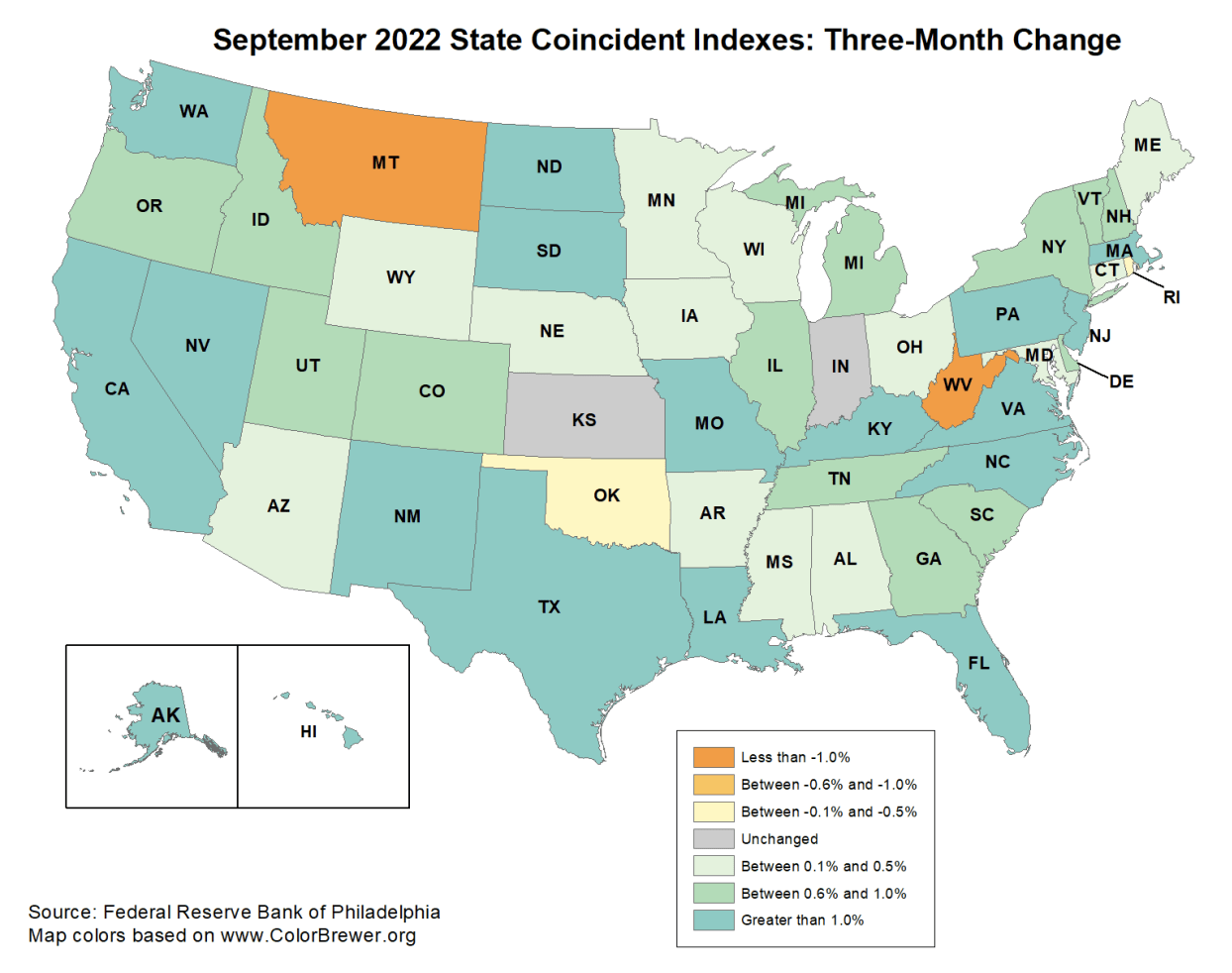

By September 2022, the cycle started to turn at the margins, but large population centers saw continued growth.

September 2022 State Level Econ Data (Philadelphia Fed)

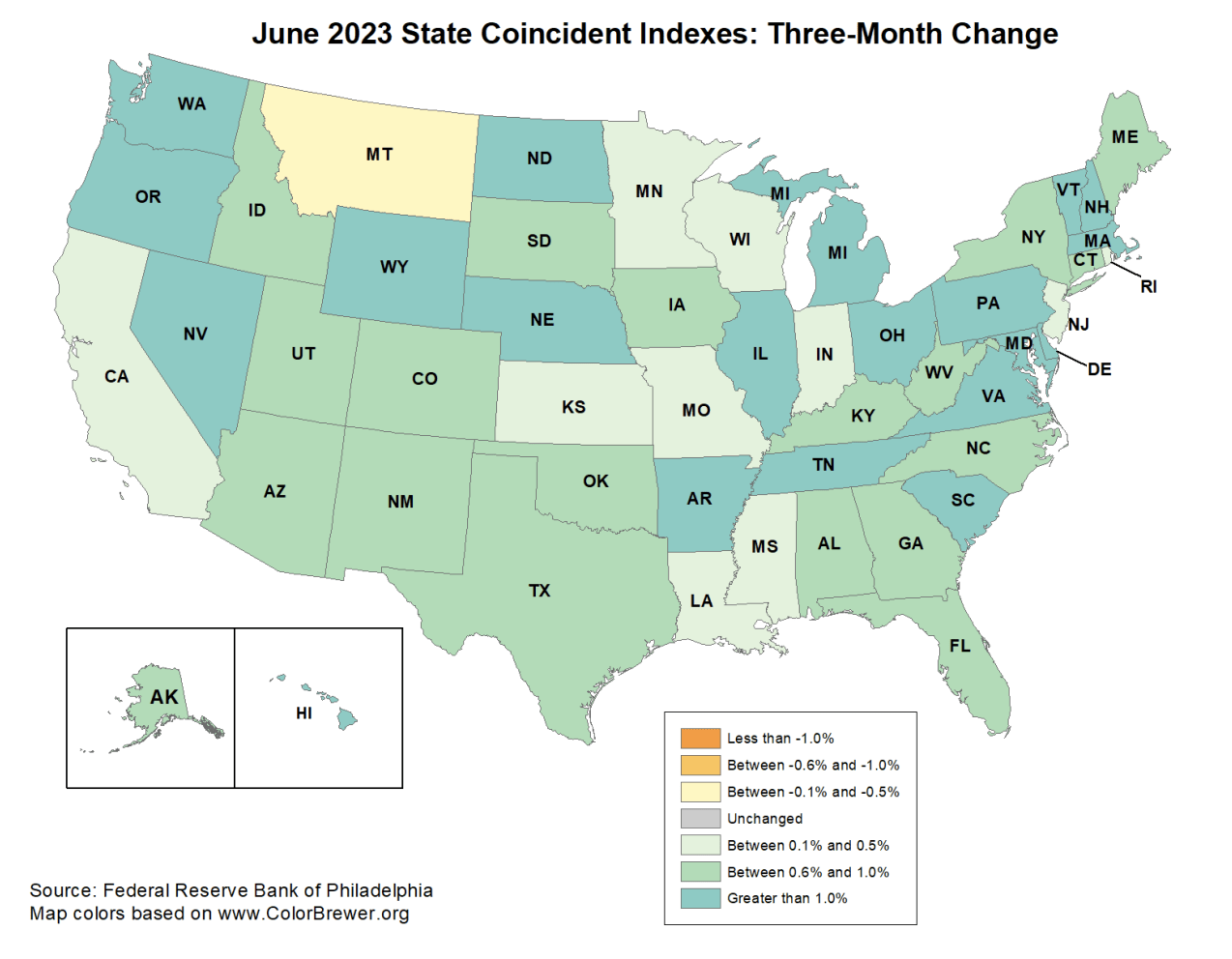

Things continued to cool in June 2023 – we see the big population centers (Eastern Seaboard, Florida, California, and Texas changing from rapid growth to slower growth).

June 2023 State Level Econ Data (Philadelphia Fed)

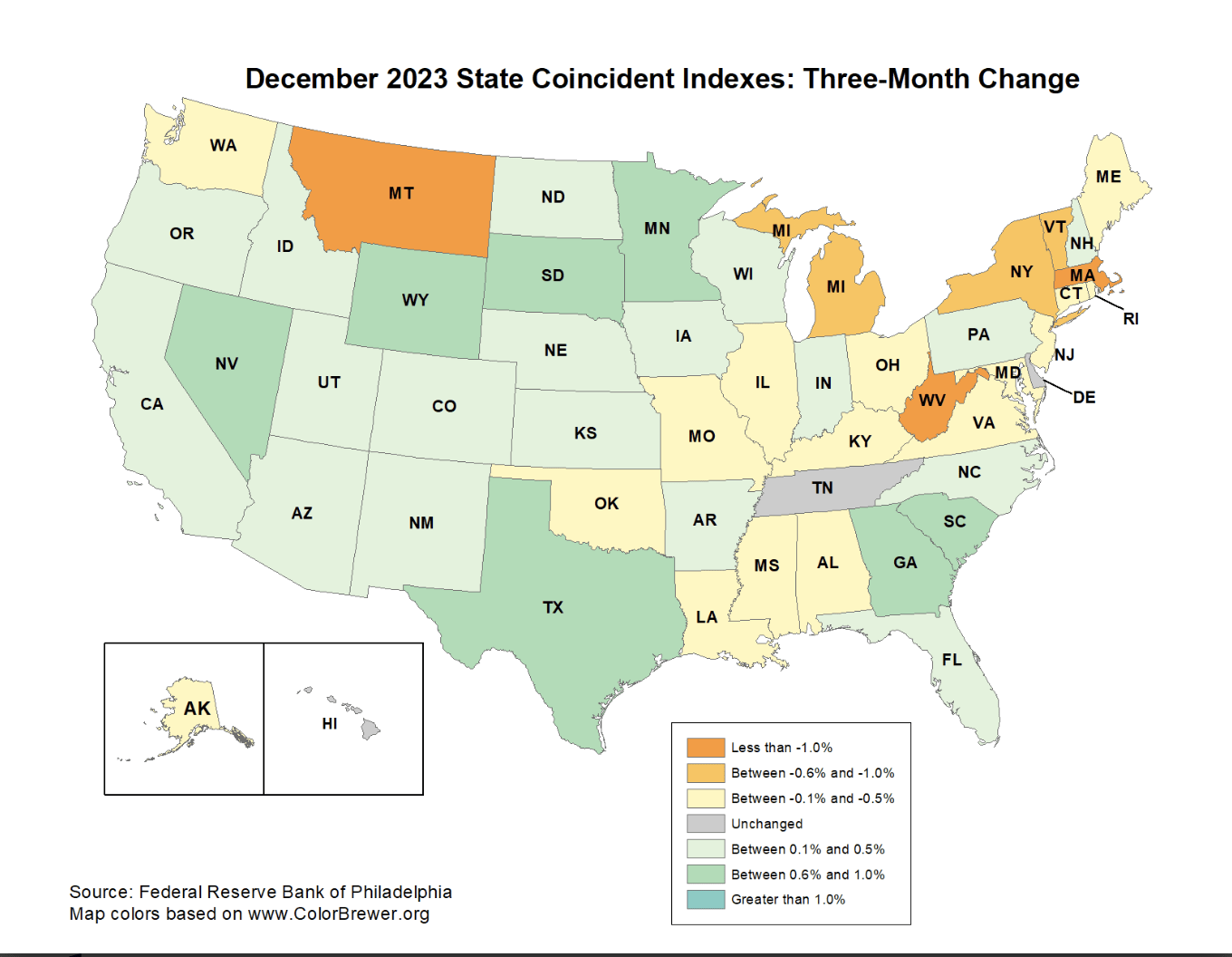

And now, we see a clear shift in the data – with the Northeast and Midwest slipping into recessionary conditions, while some Sunbelt states are holding up better.

December 2023 State Level Econ Data (Philadelphia Fed)

We don’t have Q1 data yet, but this slowdown is clear as day if you look at the leading economic indicators and higher frequency data. Data from the United Kingdom, Canada, and Australia shows that their business cycles are ahead of the US and that the global economy is cooling.

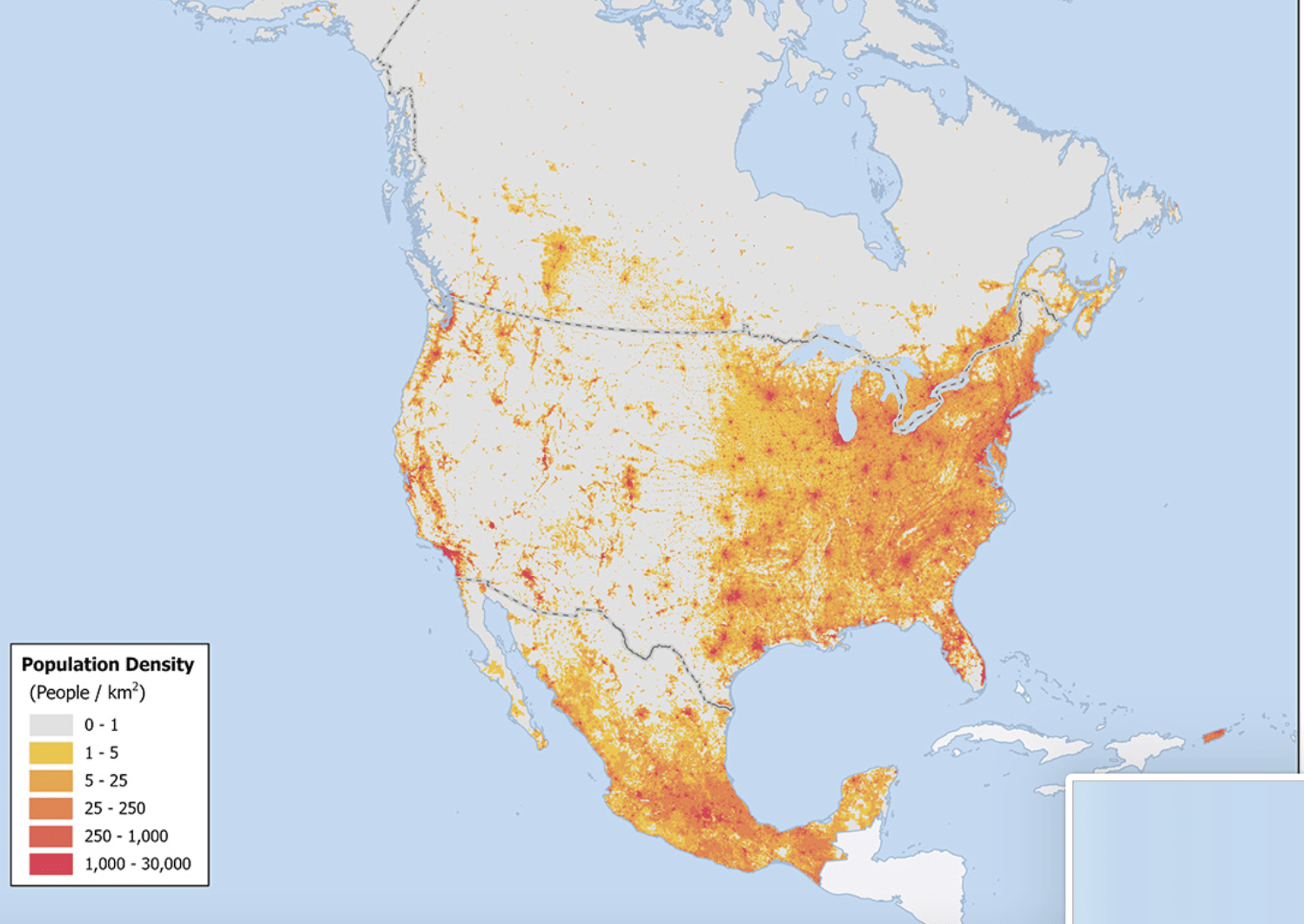

Also, the key to putting this into context is understanding that two-thirds of the population of the US lives East of the Mississippi. If you look at a population density map of North America, what you see is that these big population centers are now seeing a slow burn of job losses. Another interesting trend is toward low-wage migrant labor, with the Canadian jobs report in particular noting that their population is growing faster than the labor market.

North America Population Density (Wikipedia)

This is incredibly tricky for the Fed because I’d argue that the bubble is focused in Texas, California, and Florida, but the early job losses are happening in the Northeast and Midwest. I don’t really know how you’re supposed to set policy with this happening – there’s no way to win. The Fed tried to change bank capital requirements so they could rein in lending and speculation, but the bank industry lobby fought back like crazy, and the rules are likely to be watered down. So, like it or not, the Fed is now trying to rein in an emerging asset bubble by keeping interest rates high. The old-school thinking from the Fed is to ignore asset bubbles, but the new approach from central bankers is increasingly to push back against asset bubbles by tightening before the bubble can distort and damage the economy in the long term. This also was done in 2000 by former Fed chair Alan Greenspan, and it worked in the sense that they deflated the bubble without huge job losses. The upshot to this was that the S&P 500 went down 50%.

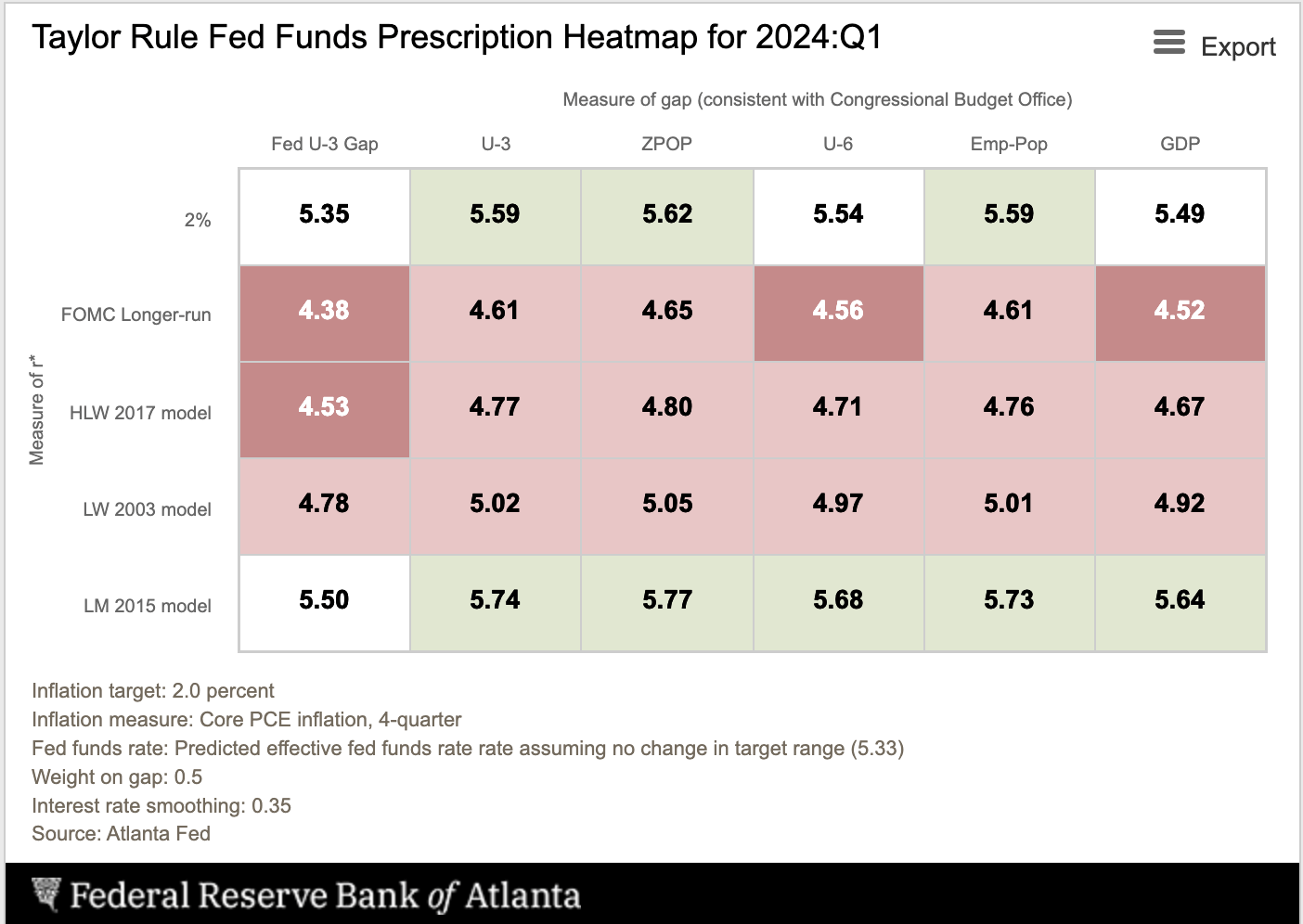

The Fed is holding interest rates at 5.5%, but a lot of the model runs using the Taylor Rule are suggesting the Fed ought to cut.

Taylor Rule Utility (Atlanta Fed)

Here, of 30 model runs, eight are suggesting the Fed pause rates, while 18 are calling for a cut. Jerome Powell got drilled by journalists about this at the last FOMC meeting, and he didn’t answer them in a way that I thought made much sense. What Powell probably knows and the journalists don’t, however, is that the Fed is intentionally keeping rates high to avoid fueling the bubble and/or another inflation surge. The Fed’s current rate policy is virtually guaranteed to create more short-run job losses in the areas of the economy that are already slowing. However, it’s also likely true that by preventing malinvestment, they’re going to set the conditions for a lower unemployment rate in the long run and a more productive economy. This is why the Fed chairman is not elected by voters. If you put elected politicians in charge they’d want to have cake for breakfast every day and fuel huge bubbles, busts, and inflation as a result.

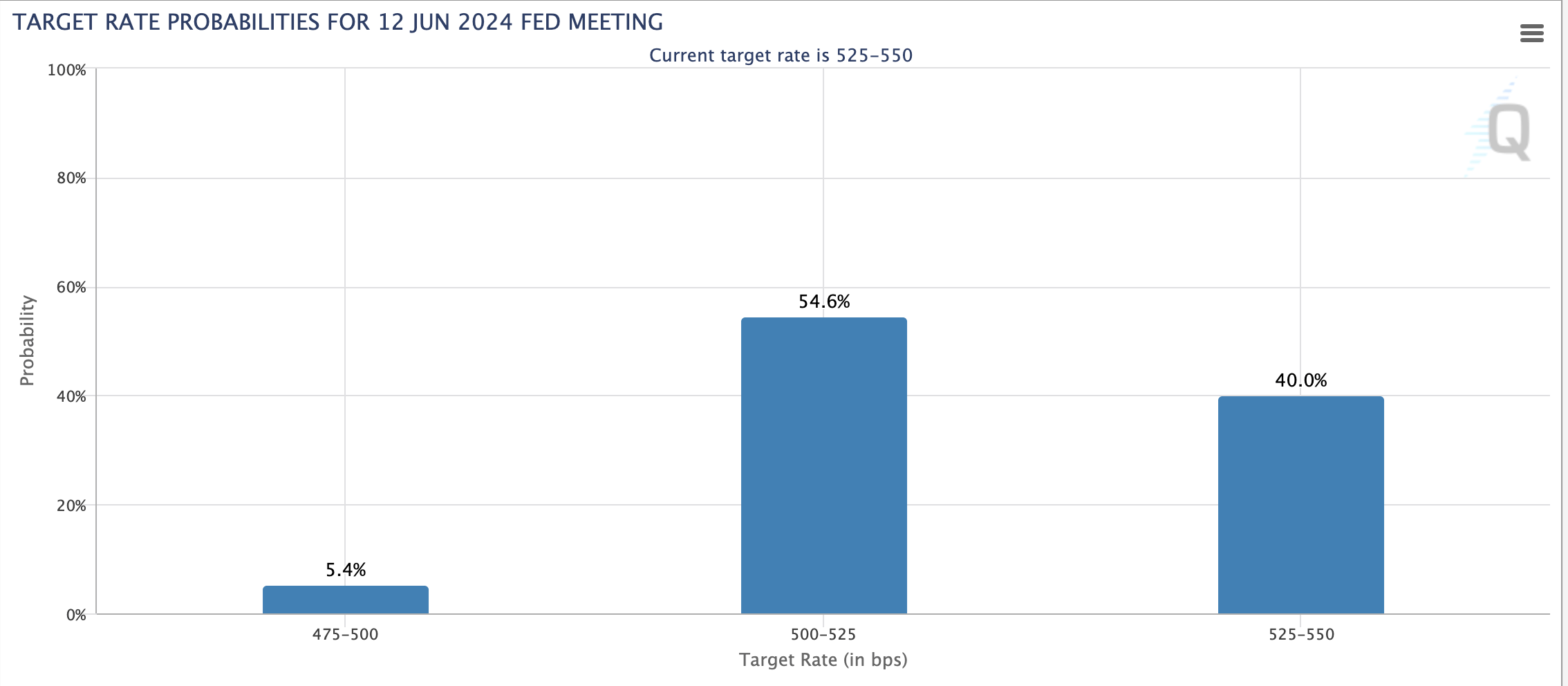

Investors currently expect the Fed to start cutting rates in June, the combination of bad inflation reports and investor exuberance might prompt the Fed to smack this idea down and keep rates high until the market gets the message.

June 2024 Fed Funds Rate Probabilities (CME FedWatch)

Investment Implications

- One of the most important things you can know as a long-term investor is that the bull market of the 2010s was mostly driven by tax cuts, 0% interest rates, and multiple expansion. This is causing investors to make assumptions about future corporate profits that are eventually going to be proven false. When this happens, the bubble will burst and stocks will likely have a lost decade. With savings rates near record lows, this could prompt some unpleasant lifestyle shifts among Gen X and Boomers.

- The Fed is willing to keep interest rates higher than necessary to rein in the current mania in stocks. This is bad for stocks and the economy but is good for those willing to hold cash.

- Stocks might offer 6% annual long-term upside at current prices but are vulnerable to a 50% drawdown if prices correct back to levels seen in the early 2000s or 2010s.

- Most people in the know seem to think that the current environment is a bubble. Jamie Dimon cited “a little bit of a bubble” in the market in a recent interview. Jeremy Grantham is reliably bearish, but his recent arguments about the bubble are worth reading. There’s a lot of central bank research over the past 1.5 years about the markets potentially being in a bubble, including from various economists at the Fed and the Bank of England. Apollo’s Marc Rowan also has warned of a bubble. Even ARKK’s Cathie Wood is taking profits. Bubble areas will be obvious in hindsight, but there are substantial mispricings in blue-chip consumer staples stocks, AI stocks, weight loss drug stocks, Sunbelt real estate, multifamily apartment construction nationwide, private credit, and junk bonds.

Bottom Line

The Fed is between a rock and a hard place with a slowing economy and a brewing speculative mania in stocks. They’ll have the opportunity to push back on market rate cut expectations this week and retake control of the narrative. I’ll be very curious to see what they do, especially given that inflation does not seem to be going away as planned. The Fed is set to update its summary of economic projections (“the dot plot”), and if they intend to drop the hammer on traders Fed pivot hopes, they’re likely to do so there and in Jerome Powell’s press conference.