Michael Vi

Palo Alto Networks Stock Suffered A Brutal Selloff

Palo Alto Networks, Inc. (NASDAQ:PANW) stock has significantly outperformed the S&P 500 (SP500) since my previous update in August 2023. While my article suggested caution then, I also highlighted that I added my exposure as PANW suffered a steep selloff following its fourth fiscal quarter earnings (FQ4 ’23). I’ve also maintained my generally bullish posture in the cybersecurity space, in line with my recent updates on Fortinet, Inc. (FTNT).

Fast-forward to February 2024, we saw another earnings-related decline in PANW. Accordingly, PANW suffered a 32% contraction from its pre-earnings February highs toward its post-earnings lows at the $260 level. I gleaned the magnitude of the decline likely stunned investors, suggesting dip-buyers likely took profit and reallocated.

Notwithstanding the negative sentiments, PANW seems to have struck a medium-term bottom as buyers returned and attempted to hold the pivotal $280 level. As a result, I assessed that it’s time for me to present an update on whether we should consider capitalizing on its near-term weakness to add more exposure.

Keen observers should be aware of the reasons attributed to PANW’s shocking release. Wedbush’s Dan Ives even called the event a “night to forget for the bulls.” Wall Street is ambivalent about Palo Alto Networks’ execution risks as it transforms its go-to-market motion. Accordingly, the leading cybersecurity company has planned to move more aggressively into its platformization and consolidation vision, capitalizing on its well-diversified solutions.

Palo Alto Networks has a highly profitable suite of best-of-breed solutions spanning network security, cloud security, and security operations. Palo Alto Networks has also made significant growth in its next-gen solutions, posting 50% YoY growth. The cybersecurity leader has also committed to its long-term goal of achieving $15B in annualized recurring revenue, or ARR, by 2030. As a result, the company believes it’s timely to address the vendor consolidation trend, in line with the increasing demands for cost optimization and ROI justification.

Palo Alto Networks Wants To Grab Share

As a result, I assessed Palo Alto Networks as engaging in a share grab maneuver in the near term as it looks to displace legacy and independent vendors. Bolstered by its market leadership in network security, it can offer a comprehensive SASE offering to its customers, strengthening its network moat effect and further entrenching switching costs. However, Palo Alto Networks management also highlighted that it observed “rogue behavior” from its competitors as they looked to defend their gains. Hence, I believe Palo Alto Networks might need to pull pricing levers in the near term to provide more incentives for customers to transition to the company’s platformization approach.

However, the move isn’t without significant execution risks. Management articulated that it has restructured its go-to-motion to include best-of-breed and platformization approaches. The latter involves longer-duration deal structures to justify more attractive pricing and incentives. As a result, I believe the market likely felt it necessary to reflect significant execution risks, as PANW is priced at a premium (“D” valuation grade) relative to its technology sector (XLK) peers.

Is PANW Stock A Buy, Sell, Or Hold?

Notwithstanding the near-term caution, Palo Alto Networks management maintained its full-year outlook for FY24, as it believes it should be able to continue gaining operating leverage. Accordingly, investors should anticipate total revenue growth of 15.5% at the midpoint and an adjusted operating income margin of between 26.5% and 27%. While the billings growth is a disappointment at 10.5% (midpoint), investors need to consider the near-term impact of its platformization strategy as it looks to invest and gain share.

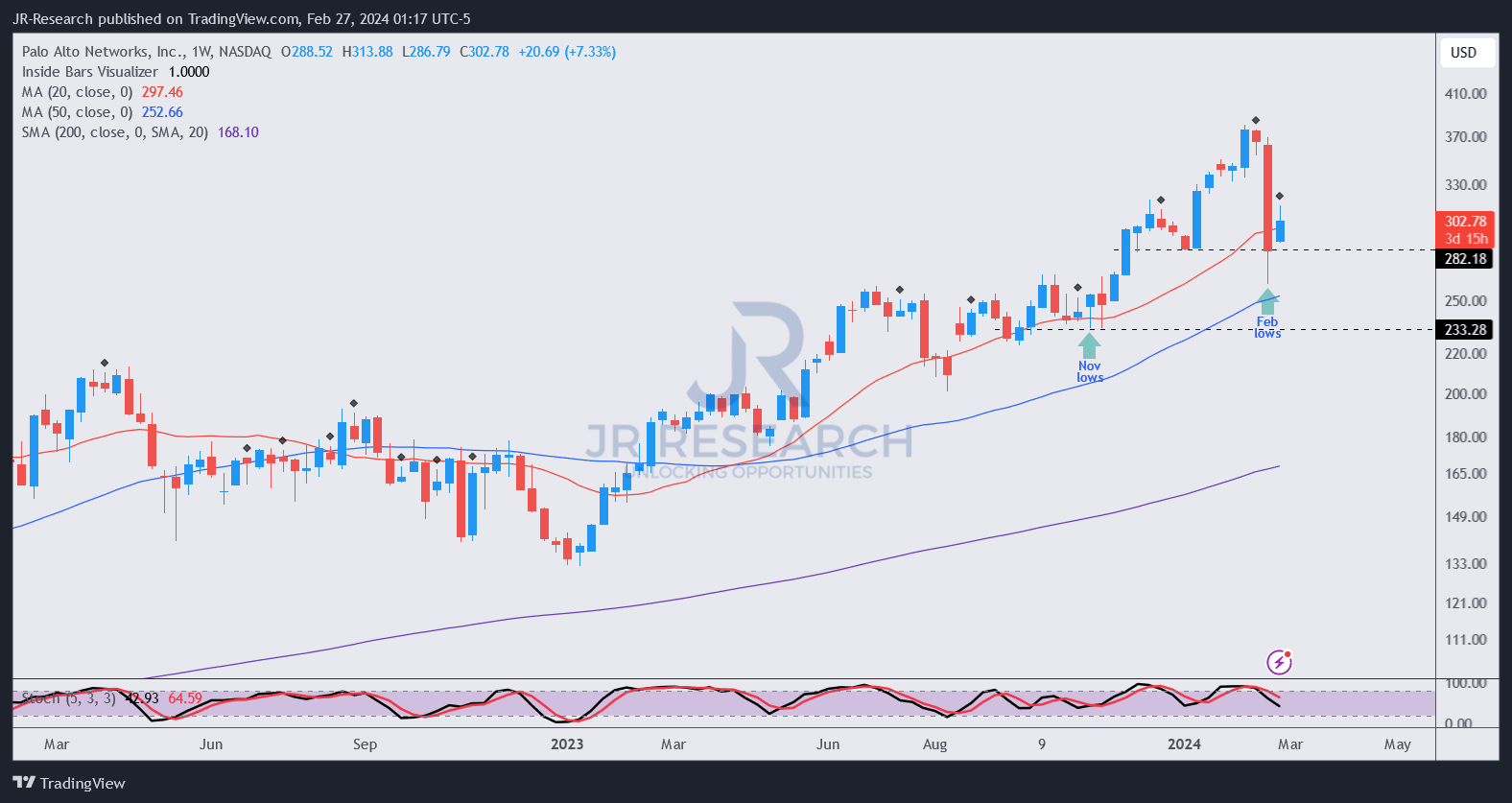

PANW price chart (weekly, medium-term) (TradingView)

PANW last traded at an adjusted forward EBITDA multiple of 37.5, in line with its 10Y average of 34.6x. In other words, PANW retraced to its long-term valuation averages at the recent decline. In addition, I also assessed robust buying support at the $280 level, underpinning its medium-term uptrend bias.

As a result, I gleaned that PANW buyers who defended the $280 level don’t seem unduly concerned about the near-term impact of its go-to-market changes as the cybersecurity leader looks to consolidate its gains. With that in mind, I assessed that the risk/reward profile is leaning more toward the bullish zone, as investors took advantage of the steep selloff to add exposure.

Rating: Upgrade to Buy.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Please always apply independent thinking and note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

I Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!