MediaProduction

Introduction

Melco Resorts & Entertainment Limited (NASDAQ:MLCO) operates resorts, hotels, and gaming facilities in Asia and Europe. On February 29, the company reported its Q4 and 2023 and at first glance, the company’s shares look attractively priced, down 45% over the last twelve months. However, upon closer revision, even assuming a meaningful rise in EBITDA over the next year, shares of Melco Resorts are deceptively cheap, as interest expenses and capital expenditures are real costs for Melco. In this article, I’ll dissect the latest results and outline why I’m staying away from Meclo Resorts for now.

Company Overview

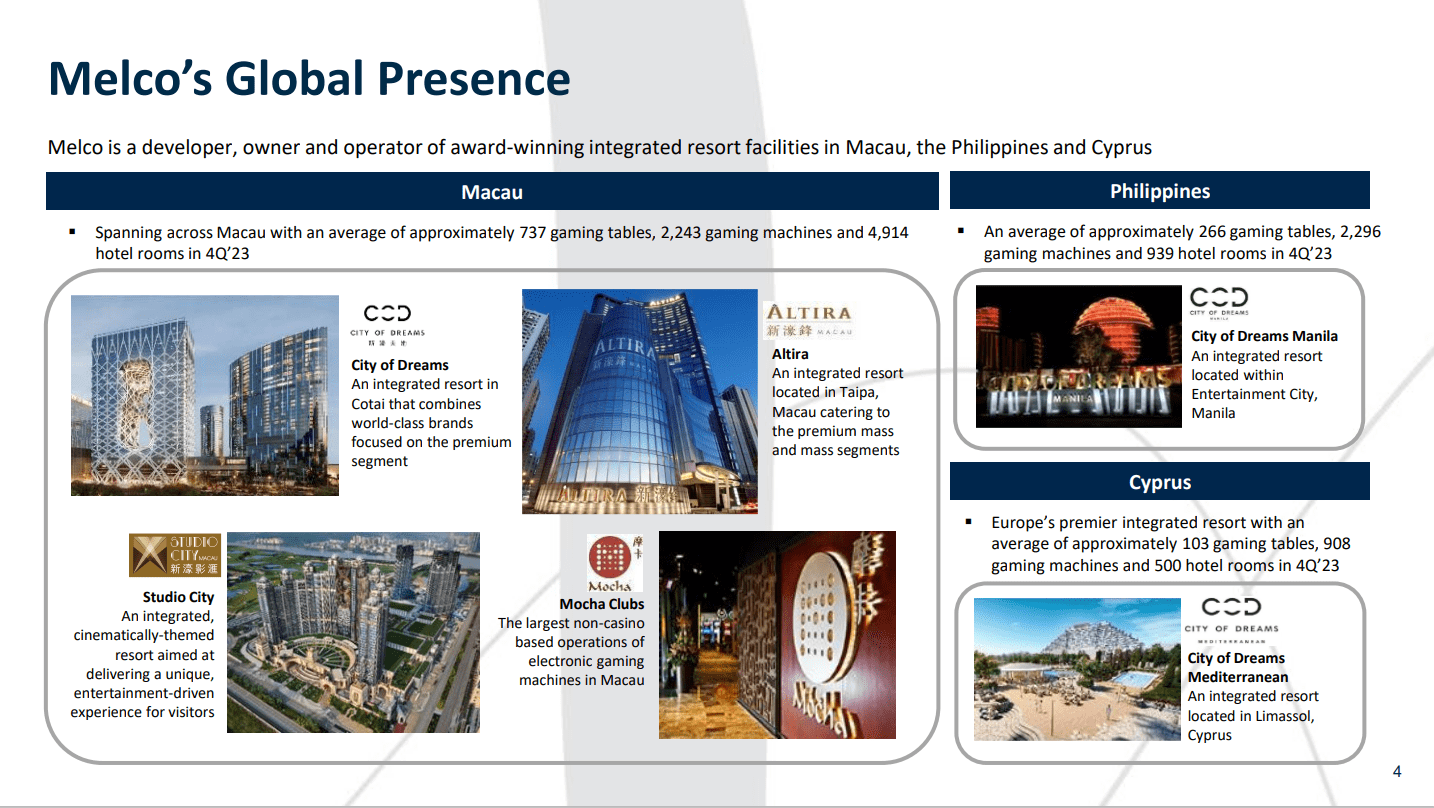

Melco Resorts is an owner and operator of resort and casino destinations in Macau, Philippines, and Cyprus. In Macau, where over half of the company’s revenues are generated, Melco Resorts has about 737 gaming tables with 4914 hotel rooms across four main properties. In the Philippines, it has a total of 939 hotel rooms and in Cyprus, where the company has some European presence, Melco Resorts has about 500 hotel rooms. Like its Macau properties, it also has gaming tables and gaming machines at these resorts too.

In addition to being a resort owner and operator, Melco’s resorts are home to a wide range of entertainment and leisure activities for its guests. In addition to gaming and gambling, it also has restaurants and bars, pools, salons, spas, and health and fitness centers at its locations. Many of its guests come from all around the world to visit these properties as a result of its amenities and entertainment features.

Investor Presentation

Background

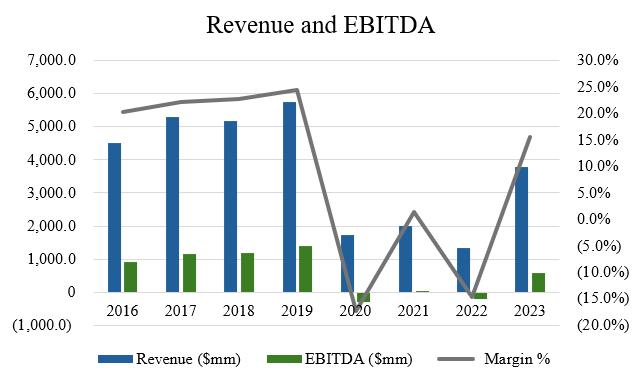

The financial performance of Melco Resorts has been lumpy, to say the least. Pre-pandemic, the company had been performing well with consistent profitability along with revenue growth in line with inflation. But after the pandemic hit, consumers no longer travelled as a result of government restrictions and health concerns, which negatively impacted demand for travel and vacations. In the case of Melco Resorts, the company had been largely unprofitable for much of the 2020-2022 period. Since then, 2023 has been somewhat of a rebound year for the company with revenue growth picking up again and restored profitability as consumers begin to travel again, with over half of Americans looking to make travel plans in 2024. Some experts have referred to this trend as ‘revenge travel’ as for the longest time people were unable to travel. This trend is expected to continue.

Author, based on data from S&P Capital IQ

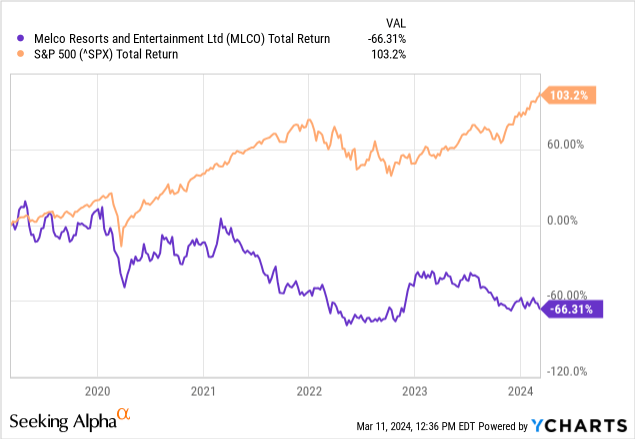

When looking at the share price performance of Melco Resorts however, despite an improving outlook for travel, the company’s shares have performed abysmally over the last year with shares down 45% in the last twelve months during a time period where the S&P500 has returned 28%. In the chart below, you can see the widening performance between the S&P500 and Melco Resorts’ stock price in the last five years, with Melco Resorts losing two-thirds of its value while the S&P500 has more than doubled, if we include dividends.

Recent Results and Outlook

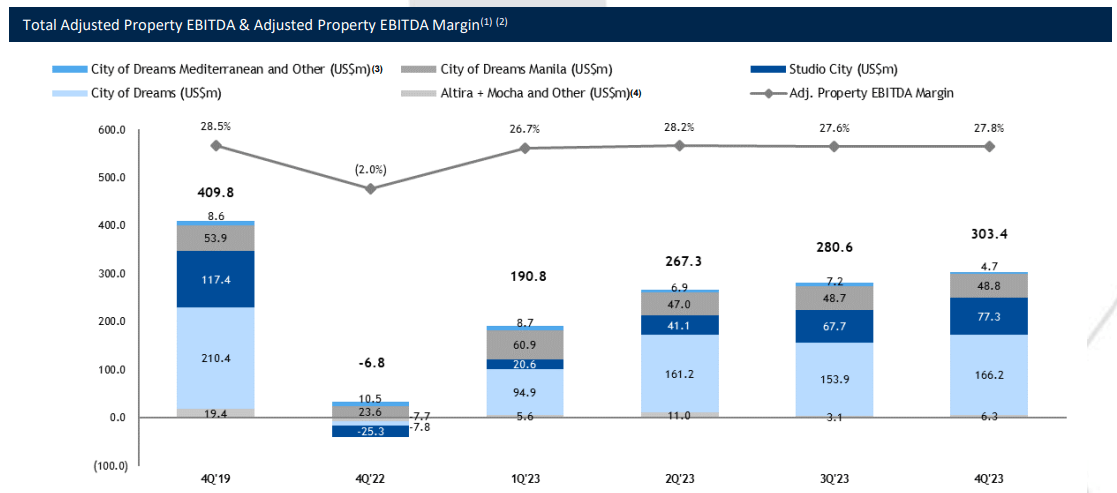

When looking at the recent results of Melco Resorts, the company reported revenues of $1.09 billion for the quarter, which was up 223% year over year, along with earnings per share of $0.36. On an adjusted EBITDA basis, the company reported $303 million in adjusted EBITDA on a 27.8% margin.

Overall, this was a pretty good quarter for Melco Resorts as the company reported its fifth consecutive quarterly increase in adjusted EBITDA. As I mentioned earlier, the company has been in the process of recovery during the pandemic and things seem to be on a slow return back to normal.

In addition, a few new developments took place that helped strengthen revenues and margins, namely the City of Dreams Mediterranean and Studio City Phase 2. In my view, these fit well with Melco Resorts’ existing portfolio as they are essentially luxury properties that are likely to attract wealthy clients with high-end services and high limit gaming facilities. On the earnings call, management noted that the ABT generated at Studio city are hitting records in terms of the funds generated through gaming (daily mass and slot GGR).

As for F2024, Meclo Resorts has a number of projects in the pipeline and underway that could be a potential catalyst for the year. For example, the Residency Concert Series at Studio City starts this month and new construction and expansion plans at other facilities should expand capacity and offerings. There are also renovations happening at the Countdown Hotel which elevates capex right now, but should strengthen the property’s position as a luxury hotel.

In Macau, a substantial majority of Melco Resorts customers come from mainland China. In 2021, visitors to Macau fell 46% compared to the prior year. Today, when looking at Melco Resorts performance, the resurgence in demand has meant that visitation to Macau was close to 2019 levels during the Chinese New Year celebratory period and total visitors from China were actually higher than what they were in 2019.

Based on Macau government reports, total visitors to Macau in 2024 are expected to be 33 million, which would represent an increase of 17% against 2019 levels. If we extrapolate 17% growth to the company’s top line at the same 27% margins, this would add nearly $46 million in EBITDA per quarter.

When looking at the balance sheet, Melco has quite a bit of debt. While not unusual for a company that owns significant real estate assets, the company does have a Net Debt to EBITDA ratio of 6.1x with $7.5 billion of long-term debt and $1.4 billion of cash. Keep in mind that I’m using EBITDA on a TTM basis as reported by the company. If we annualize Q4 to forecast out for 2024, the Net Debt to EBITDA ratio would still be around 5.1x, so clearly there are some concerns about the leverage here.

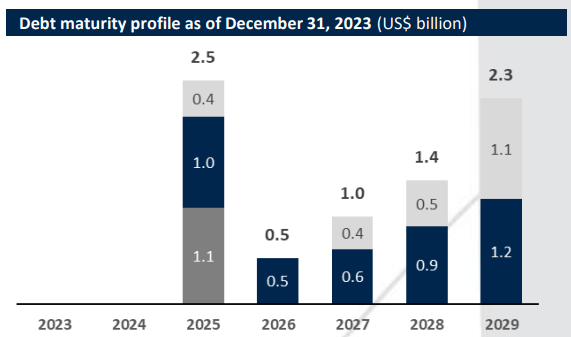

Investor Presentation

While most of the debt is fixed rated debt, the interest costs are closing in on 6% now, and a fair bit of that debt will come due in 2025. Monitoring how Melco Resorts chooses to refinance that debt and at what rate will be important to watch. Overall, total debt at the company is down about $1.0 billion compared to Q4 of 2022, so the trajectory seems okay for now.

Investor Presentation

Another thing to remember is that hotels and casinos have much higher capex compared to commercial and industrial real estate, for example. When looking at the historical capex for the company over the last five years, Melco Resorts has spent an average of $535 million on capex per year. A good portion of this is maintenance capex like renovations and repairs, and these are simply costs that aren’t going to go away. So when calculating a valuation multiple like EV/EBITDA, it’s important to keep this in mind.

Valuation

Based on the sell side ratings and target prices on Melco Resorts’ stock, there are 5 analysts covering the stock with 3 ‘buy’ ratings and 2 ‘hold’ ratings. The average price target is $11.24, with a high estimate of $15.00 and a low estimate of $9.60 (source: TD Securities). From the current price to the average price target one year out, this implies potential upside of 54%, suggesting that analysts are very bullish on the near-term outlook for Melco Resorts’ stock.

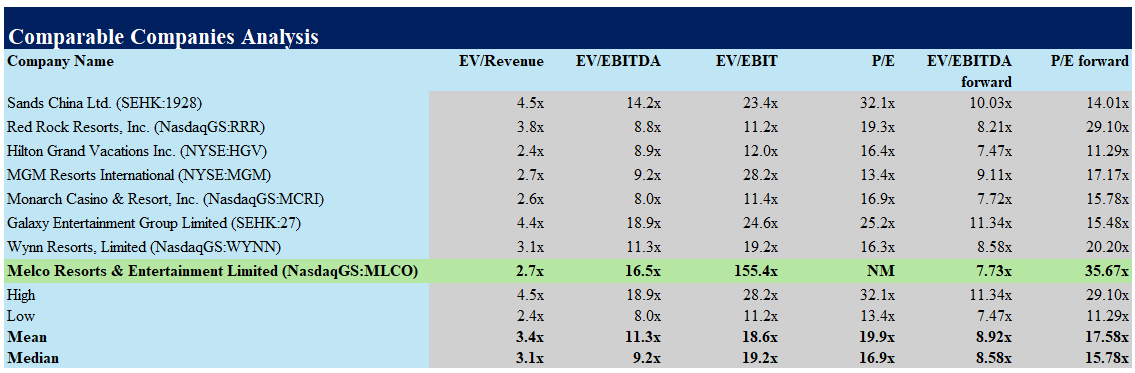

Comparing to industry peers that operate in resorts, hotels, gaming and have international presence, Melco Resorts trades at a premium on a EV/EBITDA basis when using the TTM number but trades at a slight discount to the group on a forward basis at 7.73x EBITDA (average peer multiple of 8.9x EBITDA). Overall, I think the discount is warranted due to the elevated risk of operating completely in Asia and Europe, where demand for hotels is not as resilient as shown by the pandemic. Melco Resorts’ balance sheet is also highly levered, which also poses some risks to the company.

Author, based on data from S&P Capital IQ

When looking at the EV/EBITDA ratio for the company, Melco Resorts has an equity value (market capitalization) of $3.2 billion, and $7.5 billion of long-term debt and $1.4 billion of cash, giving it an enterprise value of $9.3 billion. Annualizing the latest quarter, this gives us an EV/EBITDA multiple of 7.8x. But when deducting the average capex of $535 million over the last five years from EBITDA, this increases the multiple to 14.0x.

And that’s before any of the interest payments on the company’s debt ($466 million), share based compensation ($35 million per year), and other real costs to the company like opening costs and other corporate expenses. As you can see, the quoted EV/EBITDA multiple of 7.8x is deceptively cheap for a reason. With mounting interest payments and heavy capex, I think shares of Melco Resorts aren’t as attractive as they might appear at first glance.

Conclusion

Overall, I think Melco Resorts is taking the right steps to position itself the growthier Asian and European markets where it targets more wealthy clients and affluent consumers. Thus, so long as travel restrictions have eased now and consumers want to travel again, EBITDA should increase steadily from here. At the same time however, when accounting for the large interest and capex expenses of the company, the current EV/EBITDA multiple doesn’t accurately capture the true valuation and earning power of the business, where in fact Melco Resorts is actually much more expensive than it appears at first glance. While the company did pay down a substantial amount of debt in 2023, it will take a long time to make a meaningful dent in its overall financial obligations, especially considering the cyclical nature of the hospitality industry and potential future economic uncertainties. As such, I think there are better opportunities in the market today which is why I’m giving a ‘hold’ rating to the company’s shares.