Alex Wong/Getty Images News

The Fed has tried to push back against rate cut expectations. Still, with financial conditions easing and inflation swaps pricing in higher inflation rates coming, the Fed needs to take back control of what is happening, specifically in the equity market, where it seems like a casino-like mentality has officially taken over.

Powell This Week

This week will offer the Fed one last chance to regain control and set the stage to rein in the markets potentially and their rising inflation expectations before the FOMC meeting. That will come when Jay Powell goes before Congress on March 6 and 7.

Since the December FOMC meeting, financial conditions have eased after the Fed shocked the markets by acknowledging that there would be rate cuts in 2024. Despite hotter-than-expected January employment and inflation data, markets have refused to allow financial conditions to tighten.

Today’s credit spreads are equal to 2017, 2018, 2019, and 2021, when the real Fed Funds rate was less restrictive than today when measuring the effective funds rates versus headline CPI or core PCE, and negative in 2016, 2017, and 2018, and just slightly positive in 2019.

Bloomberg

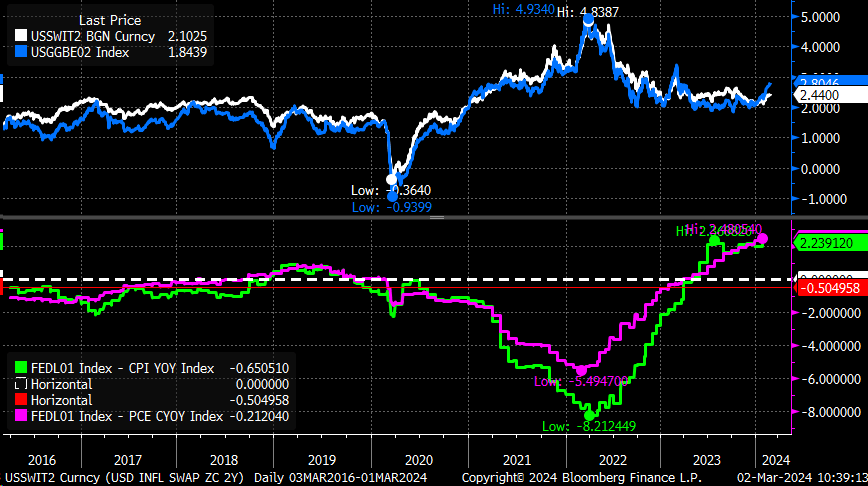

Despite today’s higher real Fed Funds rate, inflation expectations have risen in recent weeks, with 2-year Inflation Breakevens climbing to 2.8% and 2-year inflation swaps climbing to 2.44%. A move up in recent weeks, with most of the gains coming since the start of 2024. This would seem the opposite of what one would expect at this point in the cycle, where they should be continuing to moderate.

Bloomberg

Also, since the hot PCE report this week, monthly inflation swaps are now seeing the CPI y/y inflation remaining above 3% in February, March, April, May, and June. So, after a year of hearing about the disinflation process, it would seem that the inflation swaps market is saying that the disinflation process has stalled and expects inflation in June 2024 at the same level as in June 2023, increasing by 40 bps since February 14, and 25 bps since February 22.

Bloomberg

Economic Data Can Help Powell

Perhaps Powell doesn’t push back against the market and easing financial conditions, despite the recent rise in inflation pricing, in hopes that this week’s data does the job for him. After all, another hot job report, or data in general that points to higher wages or higher services inflation, could lead to rates on the long end of the curve rising, the dollar strengthening, and doing some of Powell’s heavy lifting. Another month of robust economic data could push back calls for three cuts in 2024 and shift the conversation around no rates coming.

The ISM services data is expected to come on March 5, and analysts see the services index falling to 53 in February from 53.4. Meanwhile, the prices paid piece, which seems to have called the hot services data witnessed in the CPI and PCE report, will be closely watched compared to last month’s reading of 64. The NFIB small business index noted that firms planning to increase prices have been steadily climbing over the previous few months, which does create the risk that the prices paid unit in the ISM also trend higher.

Bloomberg

The JOLTS data on Wednesday has been a highly watched number by Powell and Company over the past year. Expectations are for job openings to fall to 8.89 million in January from 9.02 million in December. However, the JOLTS data tends to be hard to predict and is subject to significant revisions. The NFIB index that tracks job openings that are hard to fill has been generally trending lower. The number of open jobs posted on Indeed has also steadily declined, suggesting that the JOLTS data should still trend lower.

Bloomberg/St. Louis Fed

Of course, the big numbers will come on Friday with the US job report, with analysts forecasting 200,000 created in February versus last month’s 353,000. The unemployment rate is forecast to remain unchanged at 3.7%, while average hourly earnings month-over-month are forecast to rise by 0.2%, down from 0.6% and by 4.3% y/y, down from 4.5%.

If the totality of the data supports the idea that wage pressures are still elevated, the job market is still tight, and services prices continue to gain. One would think that the recent gains in market-based inflation expectations could rise more and, as a result, push rates on the back of the curve higher, moving real rates higher, strengthening the dollar, and tightening financial conditions. Ultimately, having a solid economy with stable prices is a good thing and something we should all want. However, having an economy with high inflation rates is not good, and over time, it brings on even higher interest rates while decreasing overall affordability levels.

Casino Is Open

Unfortunately, a runaway stock market doesn’t help in dealing with inflation; it may even make it worse. Most think that the “market” doesn’t care about the Fed or rates, but for the most part, that is a wholly incorrect way to think about it. The correct way to think about the equity market is in terms of financial conditions and, more importantly, liquidity. When financial conditions are tight or tightening, liquidity is less ample, and implied volatility levels are higher, pushing back the animal spirits that kick in when financial conditions ease and liquidity becomes ample.

Bloomberg

Ultimately, the equity market trades with financial conditions, as noted by the relationship with the S&P 500 earnings yield and the CDX high yield index. So essentially, when credit spreads are contracting, it is bullish for stocks, and when those spreads are widening, it is bearish for stocks.

Bloomberg

So, at this point, the data will have to support higher long-term rates driven by an economy that is not cooling sufficiently to warrant rate cuts in 2024. Or Jay Powell will have to take control of financial conditions by jawboning the market back into place to ensure inflation doesn’t heat back up as markets are beginning to price in.

The most significant thing it appears the Fed is risking at this point is conditions easing even further and seeing inflation start rising again because, at least to this point, oil has been well-behaved, but that isn’t likely to last for much longer because oil is a risk-asset too. If oil starts rising, it will be a checkmate for the Fed, and the risk will swing from no rate cuts back to the risk of more rate hikes.