dmbaker

“If you buy things you do not need, soon you will have to sell things you need.”

— Warren Buffett

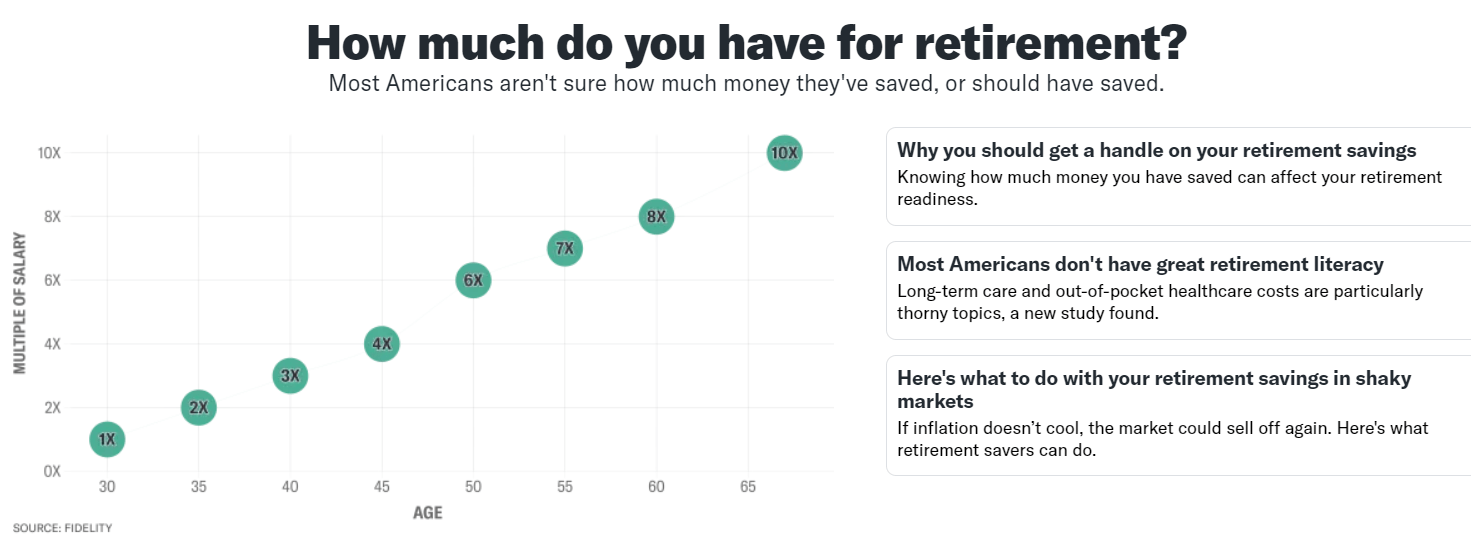

A recent post from Forbes Advisor stated that more than one third of Americans who earn more than $200,000 per year still live paycheck to paycheck, and many of them have less than $2,000 in savings. At the same time, as many as 10,000 Americans per day are reaching retirement age, according to AARP.

Every day in the U.S., 10,000 people turn 65, and the number of older adults will more than double over the next several decades to top 88 million people and represent over 20% of the population by 2050.

Just about every week, I see a story online asking those who are about to retire if they have enough to support their retirement. As I was composing this latest article on my Income Compounder approach to generating retirement income, I came across the story below from Yahoo Finance discussing how much is needed for retirement.

Yahoo Finance

Based on a report from TIAA Institute, 1 in 4 Americans do not know how much they have saved for retirement. Not only that, but one in eight Americans could not even come up with $2,000 to pay for an unexpected expense. If you are one of those 10,000 who are approaching retirement age and do not already have a plan for retirement savings, or do not have nearly enough saved yet, the time is nigh to start planning!

While nearly two-thirds of Americans have at least some money invested in retirement accounts such as 401(k)s, traditional individual retirement accounts (IRAs), Roth IRAs, and pensions, less than half of those who are not yet retired are “very” or “somewhat” confident they will retire when they plan to, according to the TIAA report; 15% don’t plan to retire at all.

Although saving for retirement is only half the battle because the other side of the equation is the expense side. To be able to determine how much you need to save, you first must estimate how much you will be spending in retirement. Because you will no longer be receiving a paycheck every two weeks, or whatever pay period you have been accustomed to, you will need to find a way to replace that income to cover those expenses.

Many 401k plans or IRAs simply show an account balance, but that balance can vary daily and does not necessarily indicate how much income will be provided to a retiree. New laws now require that the income equivalent must be included on those 401k statements, as explained in the Yahoo Finance story:

Employers who offer 401(k)s and other defined contribution retirement accounts are now required by law to include two illustrations of a participant’s account balance converted into a lifetime income equivalent — one as a single life annuity (for just the participant) and another as a qualified joint and survivor annuity (for the participant and spouse) — at least annually.

My Income Compounder Approach

With my Income Compounder, or IC portfolio, I enjoy a regular income stream from stocks like BDCs and REITs, and funds like CEFs and ETFs, that mostly pay monthly (and some quarterly) distributions. Because my portfolio holdings are based on very high yield distributions, generally exceeding 10% annually, I have a reliable and growing river of cash coming into my portfolio each month. Then I automatically reinvest, or DRIP, at least 50% to 75% of those distributions to continue growing the future income streams.

Using this approach, I have been able to generate a passive monthly cash flow that far exceeds my monthly expenses in retirement. Furthermore, I can generate that cash flow from distributions without the need to sell any shares of my holdings to capture capital gains, like growth investors must do to generate positive cash flow from their investments. Of course, if the capital gains justify selling some shares to capture those profits, that can help to boost the income as well. For the most part, however, I am a net buyer of securities, using the monthly distributions that I take as cash to purchase discounted shares of whatever income holding is on sale at that time.

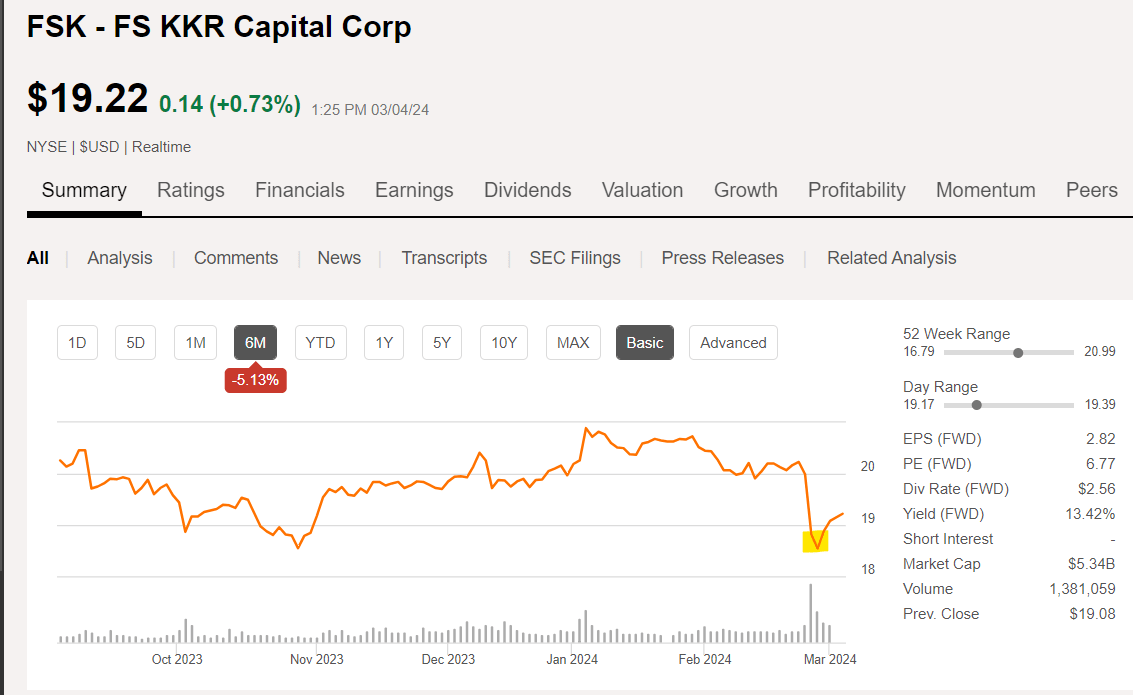

FSK

A recent example of that philosophy is based on my holdings of FS KKR Capital (FSK), a BDC stock that recently announced mediocre earnings for Q4 2023 causing the stock price to plummet the next day. I wrote about FSK back in January when I suggested that the stock was a Strong Buy at the time, when the stock was trading for $20.70. This is what I wrote in the summary of that article:

With at least two quarters worth of undistributed spillover income (based on comments made by management during the Q3 earnings call), and with over $3B in available liquidity, FSK appears to be well positioned heading into the first half of 2024.

After the Q4 report was released on February 26, the stock dropped to a price of about $18.50 before it started to rise again to above $19.20 where it trades today. I used some of the cash that I had previously received from distributions from other holdings in my portfolio to add shares of FSK while it was “on sale”.

Seeking Alpha

Despite a rise in non-accruals, FSK management suggested that the base dividend is not expected to change for the rest of 2024 and there is still another supplemental dividend to be paid in Q2. For that reason, I am comfortable adding to my shares to continue to grow my future income, but will be keeping a close eye on upcoming earnings reports.

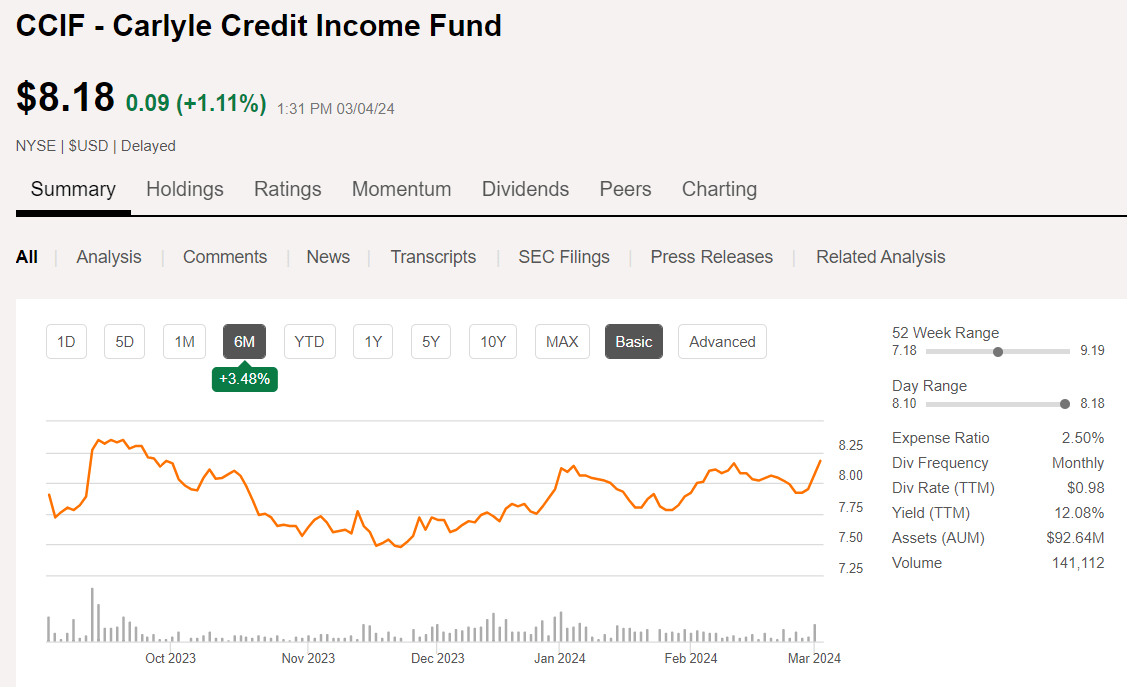

Increasing Income: CCIF

Another fund holding that I like and recently recommended that income investors consider buying for their own portfolio is Carlyle Credit Income Fund (CCIF). In December 2023, I wrote that CCIF was a successful new fund created from a troubled old one when Carlyle took over the former VCIF fund and turned it into a CLO fund. This is what I wrote in the summary at the end of that article:

I believe that CCIF is well positioned to deliver consistent high yield income from its CLO equity investments for many years to come and stacks up nicely against peers such as ECC and OXLC.

My prediction came true last week when CCIF announced the latest monthly distribution, raising it to $0.105 per share for the months of March, April, and May. That newly increased distribution now amounts to an annual yield exceeding 15% that is fully covered by NII and is due to additional CLO equity positions that the fund added during Q4 as explained in the fund’s press release.

Lauren Basmadjian, CCIF’s Chief Executive Officer said, “We are pleased with our results over the past quarter and the completion of the reallocation of the portfolio into equity tranches of CLOs, which is in alignment with Carlyle’s strategy and the fund’s mandate. With the successful deployment of the portfolio, we are increasing the monthly common dividend to 10.5 cents per share. We expect the higher monthly dividend will be fully covered by net investment income. Carlyle remains highly committed to the success of CCIF with a 41% ownership in the Fund.”

When I wrote the article in December, I rated CCIF a Strong Buy at a price of $7.73. Today as I am writing this the price has risen to $8.18 and is poised to continue rising as investors realize the massive distributions that the fund will be paying over the next few months. The fund has now gone from a slight discount to a small premium, but I would still be a buyer at this price if I did not already own a full position in my IC portfolio.

Seeking Alpha

Another Increase in Income: RIV

Another recent recommendation that I would like to remind readers about is the RiverNorth Opportunities Fund (RIV) that I discussed last month. If you are interested in more ways to increase your future income streams, consider that RIV announced in January that they are increasing the level (managed) distribution for 2024. This is what I wrote in the conclusion of that article:

The RIV fund offers income investors a steady high yield monthly distribution that is set for 2024 at $0.1289 per share. That amounts to an annual yield of about 13.5% while the fund currently trades at a discount to NAV of about -7.7%. While the discount is narrowing and the NAV is rising, I believe that there is still time to start a new position in the RIV fund for income investors who care more about receiving a steady monthly income than substantial capital gains like one would expect from a growth stock or equity fund.

In the month since that article was published, the price of RIV has risen from $11.70 to just over $12. The discount has narrowed to -4% but still offers income investors a buying opportunity to collect a steady monthly distribution that is unlikely to change for the remainder of the year even if the market suddenly retreats.

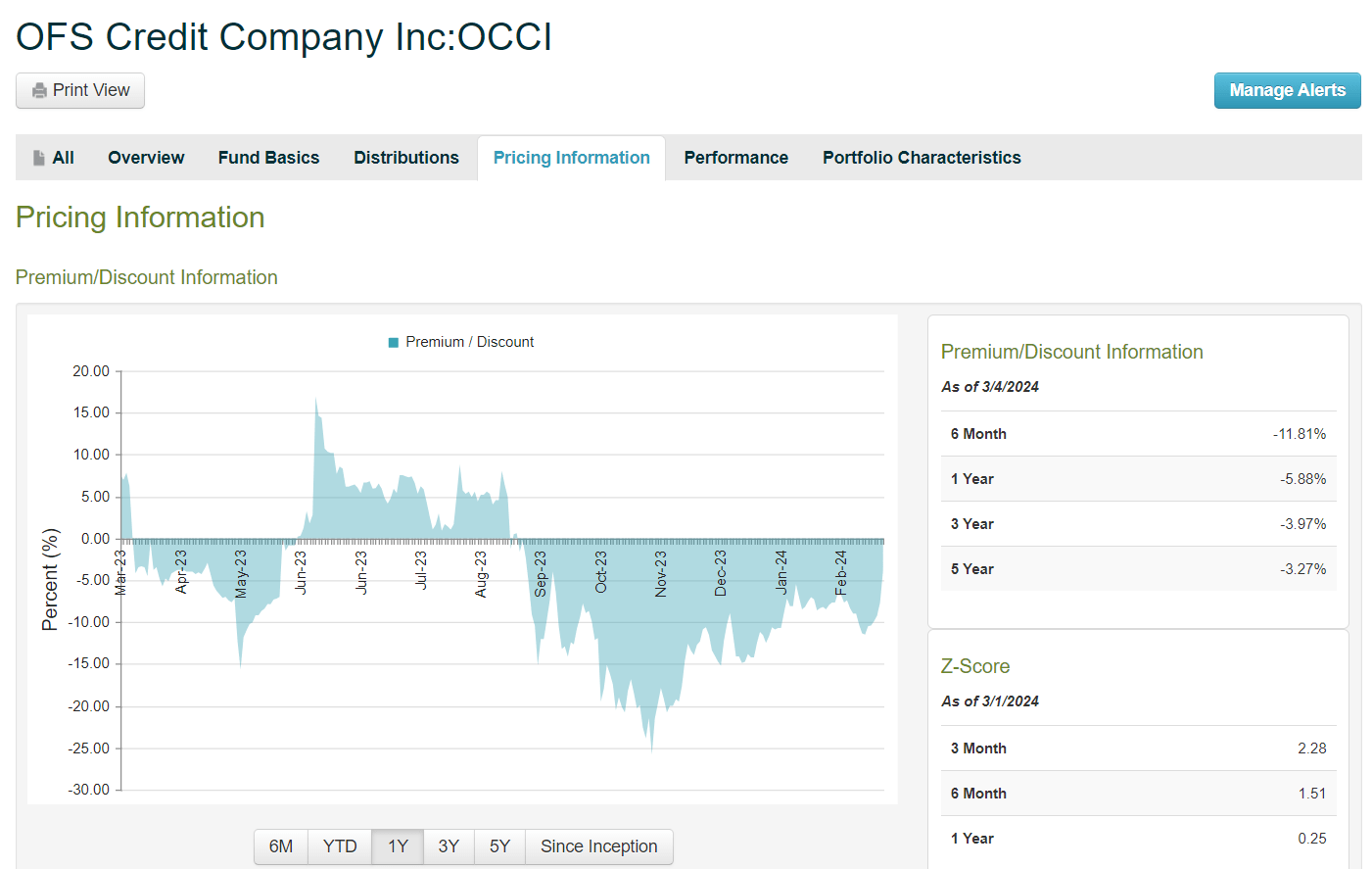

Increasing NAV Supports High Yield: OCCI

While some commenters argue that the NAV of many high yield funds just keeps dropping, offsetting the high yield distributions with capital losses on your investment, one CEF that I own in my IC portfolio has proven that theory wrong. The OFS Credit Company, Inc (OCCI) is a CEF that holds mostly CLOs and other floating rate credit instruments. According to the fund website, the team at OFS Capital Management has over 25 years of experience with structuring and investing in CLOs, debt securities, and loans.

Several analysts on Seeking Alpha have written negative reviews of the fund in the past six months, yet the fund price, cash distribution, and NAV have continued to increase since November. The chart below from CEFconnect shows this valuation graphically, with the price moving from a premium last summer to a wide discount at the end of October. That discount is narrowing now as the price of the fund increases along with the NAV.

CEFconnect

Some might argue that OCCI recently reduced the distribution when they announced last November that they were moving from a quarterly to a monthly distribution. However, in my opinion, and for my preferred purposes, the cash portion of the distribution actually increased. Because although the distribution was changed from $0.55 quarterly to $0.10 monthly starting in December, the prior quarterly distribution only paid out a maximum of 20% cash to shareholders with the remaining 80% issued in new (reinvested) shares. If an income investor wishes to reinvest the new distribution in shares instead of taking it as cash, the fund now offers up to a 5% discount to DRIP (reinvest).

On June 1, 2023, our Board adopted a change to our DRIP so that common stockholders may receive their distribution in shares based on 95% of the market price per share of common stock at the close of regular trading on The Nasdaq Capital Market on the valuation date fixed by the Board for such distribution (i.e., the payment date), providing a 5% discount to the market price.

Meanwhile, for those who wish to take the monthly distribution as cash, they would receive $0.10 per month instead of a maximum of $0.11 per quarter (20% of $0.55). Furthermore, the NAV of the fund continues to increase each month even with the $0.10 distributions being paid. The NAV is only an estimate because it is difficult to accurately calculate the market value of individual CLOs, which are essentially pools of collateralized loans. But the trend is clearly positive over the past four months, which is obviously a good trend and indicates that the fund is growing even without the issuance of new shares every month, or every quarter as was the case previously.

Seeking Alpha

At the current market price and based on a $0.10 monthly dividend going forward, the current annual yield on OCCI distributions amounts to about 16.4%. As with other CLO funds such as CCIF mentioned above, the CLO investments are paying handsome returns in 2024 that easily cover the high yield distributions without the need for very much, if any, return of capital. The increasing NAV is a good indication of that positive trend.

Summary

Passive income from investing is one way to generate cash flow in retirement. Based on my Income Compounder approach, I have offered up some suggestions for specific income investments that you may wish to consider so that you can sleep well at night, knowing that your future income stream is growing.

“If you don’t find a way to make money while you sleep, you will work until you die.”

— Warren Buffett

If you find this information useful or have anything to add, please leave a comment below. Thanks for reading, and good luck in your investing journey!

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.