RHJ

Going into 2024, one of the hottest trends was the surge in uranium prices. Throughout 2023, most energy commodities were stagnant or lost value, but uranium doubled as supply shortages grew. Although I was an early bullish investor in the uranium mining bull market, having been very bullish from 2019, the massive rally toward the end of 2023 appeared unsupported by fundamental data. In December, I published a neutral article on the uranium mining ETF, Sprott Uranium Miners ETF (URNM), followed by a bearish article on the mining giant Cameco Corporation (NYSE:CCJ) in January.

The CCJ article was nearly published at the stock’s 52-week high and the stock has lost 16% of its value since then. Of course, because many investors like the economic theories behind the uranium market (extreme demand inelasticity), my article was met with a great deal of controversy. In my experience, sharp backlash is one of the best confirming indicators of a market peak. Stocks are most often overvalued when retail investor sentiment is almost entirely one-sided.

Considering market psychology, the uranium mining complex may be in the denial phase after seeing a sharp correction. Of course, there is the potential for the uranium rally to continue, either due to a fundamental improvement in the market or, more likely, a resurgence in speculative buying activity. At any rate, I believe that CCJ remains a high-risk stock today with ample downside risk. That said, because it has faced a significant correction over a relatively short period, it is likely an excellent opportunity to reconsider the uranium market, Cameco’s fundamentals, and the technical trends facing the stock.

The Uranium Bull Market is Likely Over

The core thesis of my Cameco article was not necessarily that uranium would decline but that the company would not reap the benefits from higher uranium prices because so much of its revenue is under long-term contracts created during low-value uranium periods. I believe Cameco could only benefit from the uranium rally if the commodity remained at the $90/lbs+ level for over a year. That would only occur if there were either a permanent decline in uranium output or a long-term rise in uranium demand.

Fundamentally, the uranium commodity rally is not driven by long-term patterns; ongoing production issues and supply reductions from Cameco and Kazatomprom drive it. Those two producers control around a third of the global market share, with the top six controlling around 75%. Thus, uranium mining is dominated by a few companies with colossal production outside of the US, with only small output from Canada. In general, the uranium rally is driven by a cycle of suspended or paused production in Cameco’s Canadian operations, given those operations require a much higher uranium price to break even.

One of the most compelling bullish points about uranium is its demand inelasticity. Raw uranium costs virtually nothing to nuclear plants, and one pound supplies many megawatts of power. Raw uranium could likely cost $10K+, and it would not impact demand or even have a notable impact on nuclear power profitability, mainly driven by refining costs. Demand also changes very slowly due to changes in total global nuclear plants. The nuclear market size is expected to grow at a CAGR of 1.7% this decade. Though notable, that is not a strong growth outlook and is subject to declines if Europe reconsiders nuclear plant shutdowns. Problematically, Europe and the US have old reactors near the end of their life cycles, largely offsetting strong growth outlooks from Asia.

While uranium demand is essentially fixed, its supply curve is very elastic. I believe this is the primary overseen fact among uranium mining investors today. In the US, uranium must be above $90/lb for miners to earn a steady profit. Thus, the US produces almost no uranium despite being able to ramp up 30-40M lbs (compared to global demand of 180M lbs). That is based on past US production levels.

It may take five or more years to see that occur, but as many investors know, a large swath of US uranium mining companies are just waiting to start selling again. US uranium production did not decline due to lost reserves, but lost profitability stemming from increased exports and production in central Asia. Realistically, if uranium is in the current $90-$100/lbs range, we should see an acceleration in the uranium supply market that quickly closes the shortage. Quickly, I mean no more than two years; however, Cameco and most large uranium miners need over two years to see an impact on profits due to long-term contracting.

What is Cameco Worth Today?

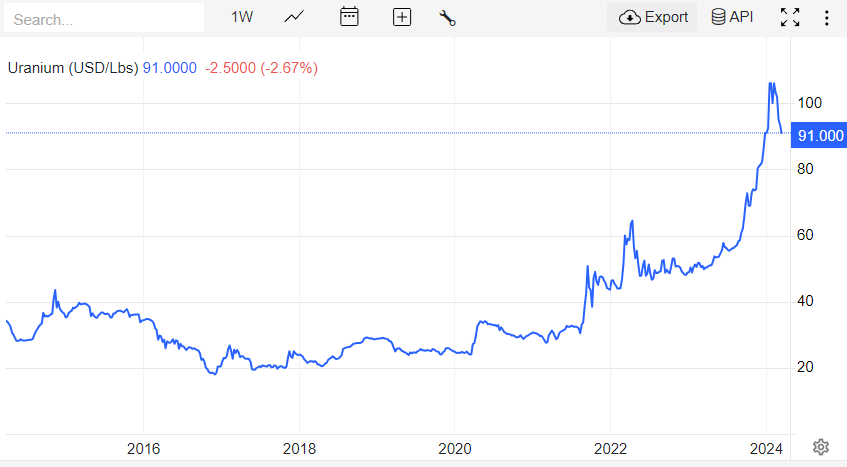

Uranium prices have reached their market peak at around $105/lb. The commodity is now down to $91/lbs and may continue to decline as the market adjusts for the supply surge from the restart to Cameco’s MacArthur/Key Lake. Three other notable US uranium miners also restarted production around the end of 2023, further increasing the supply glut. This isn’t rocket science; if supply is rising much faster than demand, prices will inevitably fall:

Uranium Price Chart (TradingEconomics.com)

Uranium’s price inelasticity goes both ways. If prices rise, the same quantity is purchased. If prices decline, demand will not rise to offset it, potentially creating a significant glut, given Cameco and other miners may not shut down production quickly enough once prices decline more quickly.

When I covered Cameco last, uranium was worth about the same. I broke down the company’s contracts and price sensitivity as well as its expected expenses, other income sources, non-operating costs, and taxes, arriving at an EPS outlook of $0.80. Slowly, positive or negative changes in the price of uranium will alter its EPS in the same direction, but primarily if uranium can maintain higher or lower prices for a prolonged period. Further, my outlook was near the middle of the analyst consensus, averaging at $0.97 (however, that may be based on January or February uranium prices).

Lastly, I agree with the analyst’s view that Cameco’s EPS will rise this decade, potentially up to the mid $2 level. Depending on how significant the total supply increase is from US miners restarting production, I expect uranium spot prices could fall back below $70 this year. That would temporarily lower Cameco’s income, likely resulting in halted output from the North American mines restarted in 2023. However, with uranium demand where it is, some North American output is needed. Thus, I expect the resting price of uranium over the next decade to be around $90 to $110, but with a scheduled correction through 2024 and possibly 2025.

In my view, uranium could only rise above that figure for an extended period if a geopolitical event blocks Central Asian exports into the US. In that scenario, uranium could quickly rise into the multi-hundred dollar range. Cameco would not necessarily benefit, however, because its main profit driver is its Kazakstan mine. From that standpoint, US miners may be a good hedge against a scaled-up conflict with Russia, but I would certainly not bet on it.

With CCJ very unlikely to earn over $1 in EPS this year and not necessarily likely to earn much more than that over the next ten, its $42 price is likely too high. CCJ is hypercyclical and has many operational risks, so I would not buy it unless at a “P/E” below 15X, likely closer to 10X. Thus, I believe CCJ is overvalued by over 50% today with a “P/E” of 42X. That said, it could maintain this price point or rise due to investor exuberance amongst the ample uranium miner retail audience.

The Bottom Line

Overall, I am more bearish on CCJ today than I was in January, as the fundamental data confirm my outlook. That said, I would not short or bet against CCJ because it could rise due to “U-Bull” investor exuberance. As a fundamentally focused analyst, I find the most challenging area to predict is the whims of speculative retail investors. CCJ could quickly rise in bullish sentiment returns, and I do not want to be on the other end of a trade against a momentum-chasing crowd. However, I firmly believe that CCJ will not maintain its current price over a long period, given its fundamental position.