PHILIPPE LOPEZ/AFP via Getty Images

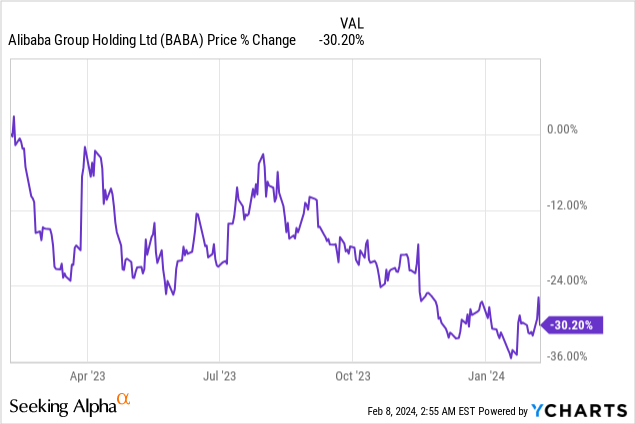

Shares of Alibaba Group Holding Limited (NYSE:BABA) fell 6% after the e-commerce company reported results for its December quarter which raised new concerns about the company’s fundamentals, especially in China. However, Alibaba’s earnings report showed a lot of promise as well and the company tried to woo investors by announcing a $25B stock buyback upsize. While China’s economy is expected to slow in 2024, I believe the company’s free cash flow looks quite good, and the buyback could allow Alibaba to buy back about 13% of its outstanding shares. Jack Ma and Joe Tsai recently bought a ton of stock for Alibaba as well and investors better take note!

Previous coverage

In my last work on Alibaba in November I called the e-commerce platform a capital return play because of the declaration of a $0.125 per ordinary share ordinary dividend. The new stock buyback of $25B is another reason to invest in Alibaba, in my opinion, as is momentum in Alibaba’s non-China e-commerce business. The e-commerce company continued to generate a ton of free cash flow in the December quarter as well and with a low P/E ratio, accelerated stock buybacks make sense. Recent insider purchases by Jack Ma and Joe Tsai are very noteworthy as well, especially in the context of a falling stock price after Alibaba’s earnings.

Alibaba’s FQ3: investors overreact to slowing top line growth

Alibaba missed Q3 expectations on the top line by $215M for the fourth quarter reported on February 7th while its adjusted EPS fell short $0.01 per share of the average prediction… mainly because e-commerce growth has been slowing in China, affecting the company’s largest business segment.

Alibaba generated 5% consolidated top line growth in the December quarter and 260.3B Chinese Yuan ($36.7B) in total revenues. This marked a 4 PP deceleration compared to the previous quarter, however, as e-commerce broadly disappointed. Alibaba’s e-commerce operations, which are consolidated in the Tmall and Taobao segments, generated only 2% top line growth in FQ3’24 compared to 4% growth in the prior quarter. The slowdown is due to economic headwinds in China and growing concerns over the property sector which have affected consumer confidence negatively. One of the largest property developers in China, Evergrande, recently was forced to liquidate its business due to a failure to restructure $300B in debt.

Alibaba’s Cloud segment also saw weak growth due to slower business spending and uncertainty about chip supplies. These trends were already visible in the preceding quarter and reason for Alibaba to delay its Cloud unit spin-off that I thought could be a catalyst and delay shares revaluing higher.

Alibaba

$25B stock buyback upsize and enormous free cash flow value

Possibly the biggest takeaway from Alibaba’s fiscal third quarter earnings release on Wednesday, in addition to slowing e-commerce top line growth, was that the company announced a $25B increase in its stock buyback. The $25B buyback will allow Alibaba, at a current price of $73.64, to repurchase approximately 13% of its outstanding shares.

The stock buyback is also backed by Alibaba’s impressive free cash flow prowess which I believe many investors are still underestimating: Alibaba is enormously profitable on a free cash flow basis and generated 56.5B Chinese Yuan ($8.0B) in free cash flow just in the December quarter. Of this amount, Alibaba returned $2.9B via stock buybacks to shareholders which calculates to a free cash flow return percentage of 37%. In the first nine months of the current fiscal year, Alibaba repurchased $7.7B worth of shares which implies a 39% free cash flow return ratio.

Alibaba

AIDC momentum

While China’s core e-commerce operations are disappointing and the outlook for China’s economic growth is muted — the IMF projects growth will slow from 5.2% in 2023 to 4.6% in 2024 — Alibaba sees solid momentum for its e-commerce brands outside of China. These operations are concentrated in Alibaba’s International Digital Commerce Group/AIDC which includes internationally-oriented shopping platform AliExpress, but also e-commerce brands Lazada, which operates in Southeast Asia, and Turkey-focused Trendyol.

Revenues in this segment soared 44% year over year to 28.5B Chinese Yuan ($4.0B) chiefly due to AliExpress seeing 60% year-over-year order growth. This growth is due to the success of AliExpress Choice which presents shoppers with a curated list of top-selling products on its e-commerce platform. Alibaba’s International Digital Commerce Group generated just about 10.1% of total revenues for Alibaba in the December quarter, so the segment is not nearly as important as the domestic e-commerce business… which achieved a top line share of 45.9%. But the AIDC segment is growing in importance — the revenue share was just 7.5% in FQ3’23 — and this is definitely a segment that is worth watching going forward.

Alibaba

Insider purchases investors should pay attention to

Jack Ma, founder of Alibaba and former Chief Executive Officer, bought $50M worth of Alibaba shares recently while Alibaba co-founder and Chairman Joe Tsai made a $150M stock buy (Source). The insider purchases, which were made in the fourth quarter, signal not only confidence in Alibaba’s growth prospects, but also in China’s economy which has been struggling to rebound from devastating COVID-19 lockdowns. Since shares of Alibaba dropped 6% after earnings, I believe it is even more important to highlight these insider purchases.

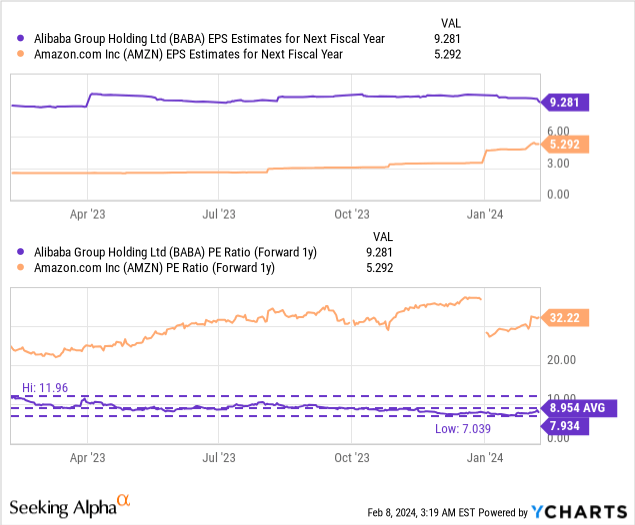

Alibaba is trading at an earnings yield of 13%

Alibaba’s shares have fallen from more than $300 in 2020 to just about $74 on Wednesday, showing a more than 75% decline in market value due to a number of factors such as a slowing economy in China during COVID-19, government crackdowns on China’s largest tech companies, restructuring efforts and a delayed Cloud Intelligence Group spin-off. However, investors appear to be too negative about Alibaba and shares are selling at a distressed earnings multiplier of 7.9X… implying a massive 13% earnings yield.

Amazon.com, Inc. (AMZN) — which is seeing a major narrative shift due to its accelerating operating income growth in e-commerce — is seeing a much higher P/E ratio of 32.2X and an earnings yield of 3.1%. The reason for this discrepancy is the high perceived risk of investing in China given the CCP’s control over the economy.

I don’t believe a 7.9X P/E ratio is appropriate for Alibaba given that the company is generating ~$8B per quarter in free cash flow. I believe Alibaba could trade at a P/E ratio of 12-13X which is a reasonable P/E range for a profitable e-commerce company that is FCF profitable and grows its top line, in my opinion. Alibaba’s implied fair value at this multiplier factor range is $111-120, implying up to 62% revaluation potential. This is a dynamic number and may rise and fall with Alibaba’s e-commerce performance especially.

Risks with Alibaba

The biggest commercial risk that I see for Alibaba is that the company has e-commerce exposure mainly in China which makes Alibaba a fairly concentrated bet on the Chinese economy… which is unfortunately expected to see slowing growth in 2024 as the property sector remains a drag on consumer spending. Despite an e-commerce expansion drive into other markets such as Turkey and Southeast Asia, Alibaba’s growth prospects will depend chiefly on the Chinese market. What would change my mind about Alibaba is if the company saw a growth deceleration in AIDC and weaker free cash flow.

Final thoughts

Jack Ma and Joe Tsai are willing to invest $200M into shares of Alibaba at a time of extreme investor hesitance, and they are teaching investors a lesson worth paying attention to: Chinese companies may not be as risky as they think, especially those companies that generate a ton of free cash flow and are growing their revenues internationally.

While Alibaba is disappointed with its top line growth in the December quarter, especially in domestic e-commerce, there are some bright spots like Alibaba’s International Digital Commerce Group which is seeing massive momentum, driven by AliExpress. The real value for Alibaba lies in its significant free cash flow and buyback power, however: Alibaba’s $25B stock buyback allows the company to buy back 13% of outstanding shares at the current price. Accelerated stock buybacks obviously make sense as Alibaba has a very low P/E ratio!