Heide Benser/The Image Bank via Getty Images

Co-authored with Beyond Saving.

Today, I want to address a question I have received before, one that I’ve seen recent articles purporting to provide. Can you create a “safe” dividend portfolio with just a handful of picks?

When I suggest that you have at least 42 different holdings in your portfolio, some readers are overwhelmed. It sounds like a lot. And it is, that’s the point. Having small allocations protects your portfolio. Naturally, people want an easy answer.

You’ve probably seen some articles that will have something along these lines:

You can have a portfolio that yields X% of “safe passive income”! Just buy these 6 holdings!

The appeal is obvious. Managing a portfolio is a time commitment. Some people enjoy playing around with investments, but for many, it is just a necessity – another chore on their list. If you can buy a handful of investments and ignore them for the rest of your life, wouldn’t that be grand? Maybe stop by once or twice a year to rebalance and forget it. Great, right?

Unfortunately, it is an illusion. I would call these “lazy portfolios.” Laziness pays off for your investments about as much as it pays off anywhere else in your life.

Lazy in your relationships? It probably isn’t going to end well.

Lazy with your house? It’s going to be a mess.

Lazy with your job? Your career isn’t going far.

Lazy with your investment portfolio? Why would you believe that would be any different?

So, when people ask me if there are a handful of funds that could replace the HDO Model Portfolio, the answer is a resounding “no.”

Don’t Be Lazy With Your Retirement

Having assets is a responsibility. If you own a car or a house, you need to ensure it receives regular maintenance. You can’t just ignore problems, hoping they go away, nor does it matter how high “quality” you buy. A very high-quality car or house might have fewer issues that need to be addressed, but it will still require time and effort from you to maintain it. Your portfolio is an asset. It is likely the most valuable asset that you own. Don’t be lazy; take care of it.

Now, when it comes to cars, many love to fiddle with them. They will tweak this or that, to get everything perfect, spending hours upon hours tinkering because it is what they enjoy. That kind of effort isn’t essential to having a vehicle that suits your needs if you just want something to get you to the store and back reliably. Many can get away just fine with checking on their car every 3-4 months, barring any indication that something is wrong.

With your portfolio, you can be a tinkerer who is constantly optimizing it. Some find that to be entertaining, but it certainly isn’t necessary. However, if you choose to manage your own investments, it is going to require some time commitment. You can’t go to the other extreme. There is no such thing as a portfolio you can just buy and ignore for decades while expecting good results.

Fooled By Backtesting

These “lazy” portfolios will often provide backtesting, look at current yields, and extend the recent performance into infinity and beyond. The real world isn’t so neat.

I like to use backtesting as much as the next guy. However, backtesting isn’t useful for telling you which specific investments are great to buy right now. By definition, backtesting tells us which investments were best to buy in the past.

When backtesting, we should be looking for the lessons to be learned about why some investments were successful. How changes in our portfolio balancing, construction, or withdrawal habits can impact our returns. It isn’t about the specific stocks; it is about the recurring themes.

One recurring theme we should learn from history is that it is a huge mistake to assume that the current economic environment will persist indefinitely. Things are always changing.

Usually, these lazy portfolios will consist of a few diversified ETFs, maybe a more concentrated fund or two, and a couple of individual stocks that have performed exceptionally well recently. Since there are only a handful of positions, the allocations will be very large; 20-40% for each fund, and 10%ish for individual stocks.

Is this a good idea? No. It is a terrible idea.

Let’s look at the components that are typically recommended in a lazy portfolio.

Funds Don’t Provide Stable Dividends

Let’s start with the biggest portion of the allocation for these lazy portfolios, which is usually a dividend-focused fund. The popular ones right now are Schwab U.S. Dividend Equity ETF™ (SCHD) and JPMorgan Equity Premium Income ETF (JEPI). Note that the “popular” funds never seem to be the ones that went through the GFC. The most popular funds tend to be the youngest funds that got started on the right foot with a period of relative outperformance. We wouldn’t want to inconvenience our backtesting with a real recession!

Funds aren’t magical, the dividends they pay reflect the underlying total return of the assets they hold and the investment strategy they employ. These aren’t companies that build a business that creates value that could continue growing indefinitely. They invest in a group of assets and they provide the total return to you. That total return will come in some combination of growing NAV and dividends.

It is a zero-sum game. While the manager of the fund can pursue a variety of strategies for determining the dividend, every dividend paid comes directly out of NAV, and every penny of gain that isn’t paid in dividends grows NAV.

As a result, you have some funds that will pay substantially all of their gains as dividends and others that will retain a large amount of their gains and pay out only a portion in dividends. If the underlying assets go through a major selloff, funds are often faced with a choice of reducing the dividend, or selling assets which risks permanent impairment of NAV. Often reducing the dividend is the best choice for the future of the fund. When the underlying assets start doing better, the dividend can then rise back up if the fund avoids selling too much when prices are low. This is why dividend cuts from funds are less concerning than a dividend cut for a company. But it is also why we shouldn’t assume that a fund’s current level of dividends will continue forever.

Understand the type of variation you might expect from a particular fund. A fund like JEPI has an inherently volatile dividend because they are relying on a type of covered call strategy. A strategy like that will lead to highly variable distributions.

Something like SCHD pays a lower current distribution, but with a diversified portfolio, the income it produces can be expected to be relatively stable; that doesn’t mean it is invincible. S&P 500 indexes saw dividends reduced by about 20% from 2008 to 2009. SCHD wasn’t around back then, but it would be fair to expect something similar.

So, if you are going to throw 30-40% of your portfolio into a fund, make sure you understand the inherent volatility potential in the dividend. If you are buying something like JEPI, understand that the dividend will be extremely volatile.

Consider an older fund that uses a covered call strategy, BlackRock Enhanced Equity Dividend Fund (BDJ). The distribution is high now, but someone who invested in 2006 has seen anywhere from an 11% yield to a 4.4% yield on their original investment over the years: Source.

Portfolio Visualizer

If you are relying on it for income, that is a big deal. If it represents 30% of your portfolio, that could be catastrophic. If you have 42+ holdings and a portion of your portfolio is dedicated to these more variable income options, maybe they are a great fit for you.

The bottom line is that funds are going to provide broad, diversified exposure to the market, often with a bias towards a certain type of stock. Your total return from a fund is going to approach “average” for whatever class of assets the fund invests in. Any dividend provided from the fund is going to reflect the total return.

Sprinkle In Top Performers – But Which Ones?

After choosing a couple of large funds, the “lazy” portfolio will sprinkle in a couple of “blue chip” stocks. “Blue chip” is generally defined as stocks that have materially outperformed over the past decade. The big benefit of these is that when you are backtesting, having a 10%ish allocation to a stock that killed it the past 10 years will boost your results.

This is essential when portraying a lazy portfolio that outperforms the indexes because large ETFs generally won’t outperform the indexes. With significant diversification, an ETF is going to see its performance approach the performance of the indexes. After fees, performance is usually slightly lower than indexes, since ETFs usually are not actively managed.

For example, from 2010, you could match the S&P 500 by putting 15% of your portfolio into Apple (AAPL) and the other 85% into a cash alternative like PIMCO Enhanced Short Maturity Active Exchange-Traded Fund ETF (MINT): Source.

Portfolio Visualizer

So if you throw AAPL in at 10% of your portfolio in any backtesting and the rest of the 90% of the portfolio just has to beat cash by a little bit for the portfolio to outperform the S&P 500.

Such winners are easy to find in hindsight. FAANG, FAANG+, “The Magnificent 7”, the “mega-caps” – whatever you choose to call them, have done extremely well in the past decade. They are the largest companies in the market by market capitalization, and investors who bought them in the past have done extraordinarily well.

So, should you just buy the five largest stocks in the market today and call it a day?

The Big Dogs Change

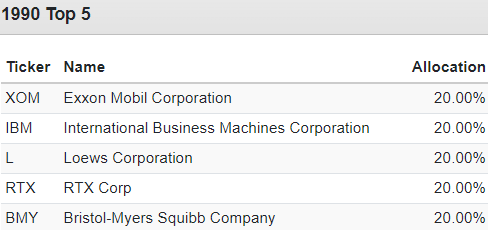

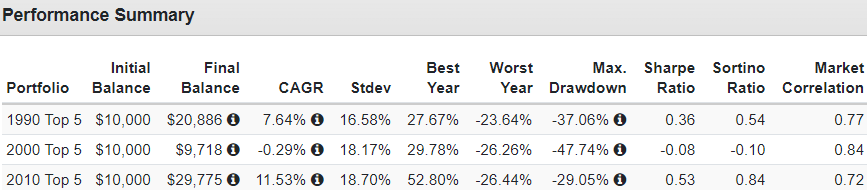

The top companies today haven’t always been the top. In 1990, here were the largest five companies: Source.

Portfolio Visualizer

These were the “blue chips” of the era. The “safe,” routine outperformers. All of these companies are still in business today, but their stock performance has been remarkably average, with a CAGR of 10.47% from 1990 through 2023, compared to 10.11% for the indexes.

These five went through periods of outperformance and underperformance. From 1990-1999, the 1990 Top 5 underperformed the indexes by a significant amount.

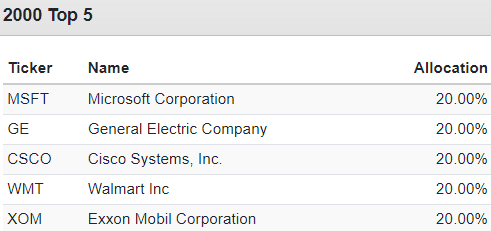

If you go back to 1990, you don’t want to buy the 5 stocks that were the largest in 1990; you want to buy the 5 that were the largest in 2000! That group consisted of these names:

Portfolio Visualizer

Only XOM hung onto a spot in the top 5. And this group crushed the 1990s. Here is their total return from 1990 through 1999:

Portfolio Visualizer

With 47% CAGR and a maximum drawdown of less than 10.5%, the 2000 Top 5 had outstanding performance in the 1990s. Hence, this is why they became the top 5 largest companies in the market.

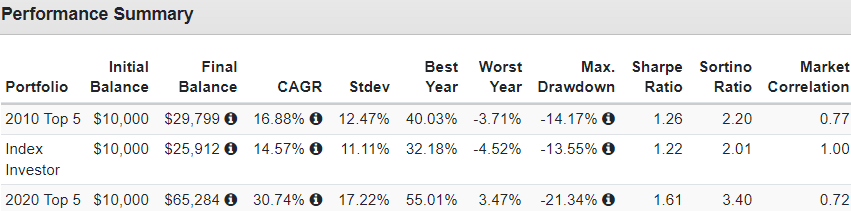

What happened from 2000-2009? The 1990 Top 5 outperformed the 2000 Top 5! But what you really wanted to own was the 2010 Top 5: Source.

Portfolio Visualizer

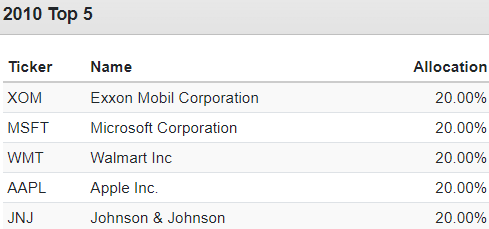

Here are the tickers that made up the 2010 Top 5:

Portfolio Visualizer

(note JNJ was actually #6, but Alphabet (GOOGL) didn’t start trading until 2004, so it couldn’t be measured over the full period)

Only XOM made all three lists; MSFT and WMT made the list twice. Today, XOM has fallen to 15th on the market-cap list.

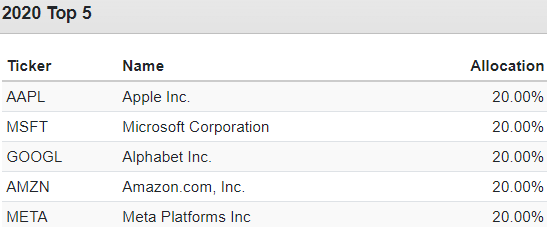

From 2010 through 2019, the 2010 Top 5 held up well, outperforming the indexes, but were nothing next to the 2020 Top 5: Source.

Portfolio Visualizer

The 2020 list is widely recognized. This list is now the list from which many people are choosing for their “lazy” portfolios:

Portfolio Visualizer

How many of these companies will be in the Top 5 in 2030? History suggests that 1-3 of them will be there. Meta has already been knocked off the list, with NVIDIA (NVDA) claiming spot #5. Those that stay on the list by 2030 are even less likely to stay on the list by 2040.

Staying at the top of the list requires a rate of growth that is simply hard to maintain for an extended period. As investors are happy with the results, they bid up the price, increasing the valuation and demanding even better results in the future. To maintain share price growth, the company needs to provide results that are even better than shareholders are already expecting. Sooner or later, the company simply won’t be able to outperform the exceedingly high expectations. This is why periods of extreme gains are often followed by periods of startling mediocrity. The more extreme the gains have been in the past 10 years, the more you should assume they won’t be repeated in the next 10.

So when constructing a “lazy” portfolio and choosing stocks based on recent very large returns, use caution. Especially if you are picking only one or two of them, the historical performance will often not be repeated. Instead, transport yourself back 10-15 years ago, would you have bought that stock before knowing it was going to be great? If you are going to try to hit the “home run” style of stock where one holding dramatically outperforms, you need to identify the ticker that is going to be huge in 2040 today. If you are buying 30-40 Growth stocks, maybe you have a fair chance of owning a couple of them. If you are buying just one or two individual tickers, I’d suggest that you are relying on extreme luck to be holding one of the true outperformers in 2040.

Diversify To Save Time?

Some people think that the more investments you own, the more time you need to put into your portfolio. True, acquiring 42+ investments does require a lot of upfront work. However, maintaining it is much less effort.

Why? Because of the relative value at risk. You need to watch a portfolio with half a dozen holdings a lot more closely.

If you have 42 individual holdings and one completely flops, you would lose at worst 2-4% of your portfolio. The overall market routinely swings 1-3% in a single day. In other words, a complete disaster puts at risk an amount that could be made up in a single good day in the market. So if you were following Roald Amundsen’s path to the South Pole, climbing Mount Everest, or sailing across the Pacific Ocean and completely ignored your portfolio, even a few holdings melting down isn’t going to ruin your retirement.

If you have six holdings, suddenly, one investment blowing up could be 10-30% of your portfolio. In other words, one bad investment could become the equivalent of your own personal bear market. It potentially puts your entire retirement at risk. With that much on the line, you better be paying very close attention to that one company and pray that it isn’t the next Enron. You need to know every relevant news item to the companies you hold because if any one investment falters, your entire retirement is at risk.

With a well-diversified portfolio, you can get away with checking in on your holdings once a quarter or so. Spend some time reviewing earnings, and if you see any red flags, dig a bit deeper and see if the company is one you still want to invest in. The risk you carry for being wrong about any single investment is greatly reduced. You still need to spend time managing your portfolio, but the urgency to act quickly is greatly reduced as the consequences to your portfolio from any single investment are greatly reduced.

There simply isn’t a replacement for diversification. You don’t diversify because you know which companies are going to bomb in the future; you diversify because you don’t know which ones will.

Conclusion

We’ve written several articles where we have done backtesting. Let me be clear: the examples used in those articles are not meant to suggest that a particular pick should be bought because of its performance over a certain period. Future performance will almost certainly be different – it could be better, it could be worse. A stock being up X% over a certain period is the weakest argument for buying any investment.

It is nice to have a track record, but it is far more important to understand why the price went up. Did earnings rise? Are the relevant economic conditions similar or different today? What conditions have historically caused the investment to outperform or underperform? What performance do you expect for the future? Backtesting cannot replace these questions.

However, we can learn a lot by looking at the past. Today, we learned that the top performers tend to change every decade. In a recent article, we used backtesting to better understand the level of volatility we can expect to experience with our types of holdings.

Backtesting is an awesome tool that computers have made available to us. Being able to process large amounts of data on individual stocks and see how changing the withdrawal level would have impacted a portfolio can go a long way toward helping us understand healthy portfolio management practices.

However, we must always remember that past performance does not guarantee future results. We should not project what has happened in the last 30 years forward to the next 30. The future will be different.

It is important to always keep your eye on your goals, and make sure that your portfolio is achieving your goals. From time to time, you will need to make changes in your portfolio to adapt to a changing economy. There is no easy button; there are no shortcuts.

Yes, you can create a portfolio that will create a massive flow of income into your portfolio, but like all good things in life, it will require effort from you. At our Investing Group, we provide education and a variety of tools to help you, and we provide our research on a wide variety of high-yield investments to make it easier.