Fokusiert

Investment Thesis

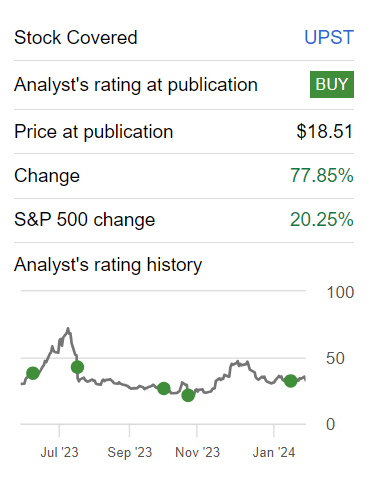

Upstart Holdings (NASDAQ:UPST) delivered its highly anticipated Q4 2023 results. And I’m left with two choices.

An easy choice and a difficult choice. The easy one is to double down on my proclamations that Upstart is worthwhile investing in.

Whereas, the difficult choice comes about when your reputation is on the line and you must act. And do so decisively. And it’s this second route that I’ve taken.

Despite the challenge of admitting that I was wrong on Upstart, I prefer to face my shortcomings now, rather than spending months looking back to its $26 per share wishing I had acted with more conviction at the time.

Consequently, I’m now calling a day on Upstart, and turn neutral on this stock.

Rapid Recap

A year ago I wrote, This is a Contrarian Bet, when I recommended to you Upstart, having been neutral on it for some time leading up to that date.

Author’s work on UPST

At the time, the share price was just under $19. Today, including the premarket drop, the share price is just over $26 per share. So, why have I decided to now turn bearish on this stock? Because Upstart is one of those businesses that is high on promises and low on delivery.

The one aspect that I’ve consistently stated has been, to watch Upstart’s debt levels. Indeed, even two weeks ago in a bullish analysis, I had stated as much when I said:

The bull case is relatively straightforward. I argue that in 6 months, once its fundamentals have stabilized, investors will be clamoring for this stock, as a fallen angel that is once again investable.

While the bear case is even more straightforward, if Upstart’s borrowing on its balance sheet is higher than $1.2 billion, I will call it a day on being bullish on this stock.

This is a highly contentious stock. And I believe it has been a lonely journey to hold a contrarian bullish view of Upstart. But alas, this now comes to an end now, as I step to the sidelines and call it a day on this stock.

Why Upstart? Why Now?

Upstart uses advanced technology, including artificial intelligence, to assess borrowers’ creditworthiness quickly and accurately. This means that they can offer loans to a wider range of people, including those who might have been turned down by traditional banks.

Upstart aims to make the loan application process faster, more efficient, and more accessible for borrowers.

In the near term, Upstart faces a complex set of challenges stemming from the broader lending landscape. The macroeconomic environment poses a significant hurdle, marked by historically high interest rates, increased consumer risk, and a cautious lending industry.

The aftermath of multiple bank failures has fueled an environment of extreme conservatism among lenders, amplifying the difficulty for Upstart in securing capital.

While remaining cautious about the near-term outlook, Upstart aims to leverage increased efficiency, as evidenced by a 26% reduction in headcount. The emphasis on extreme automation, with 89% of unsecured loans approved through fully automated processes, reflects this stance.

Given this context, let’s now jump into its fundamentals.

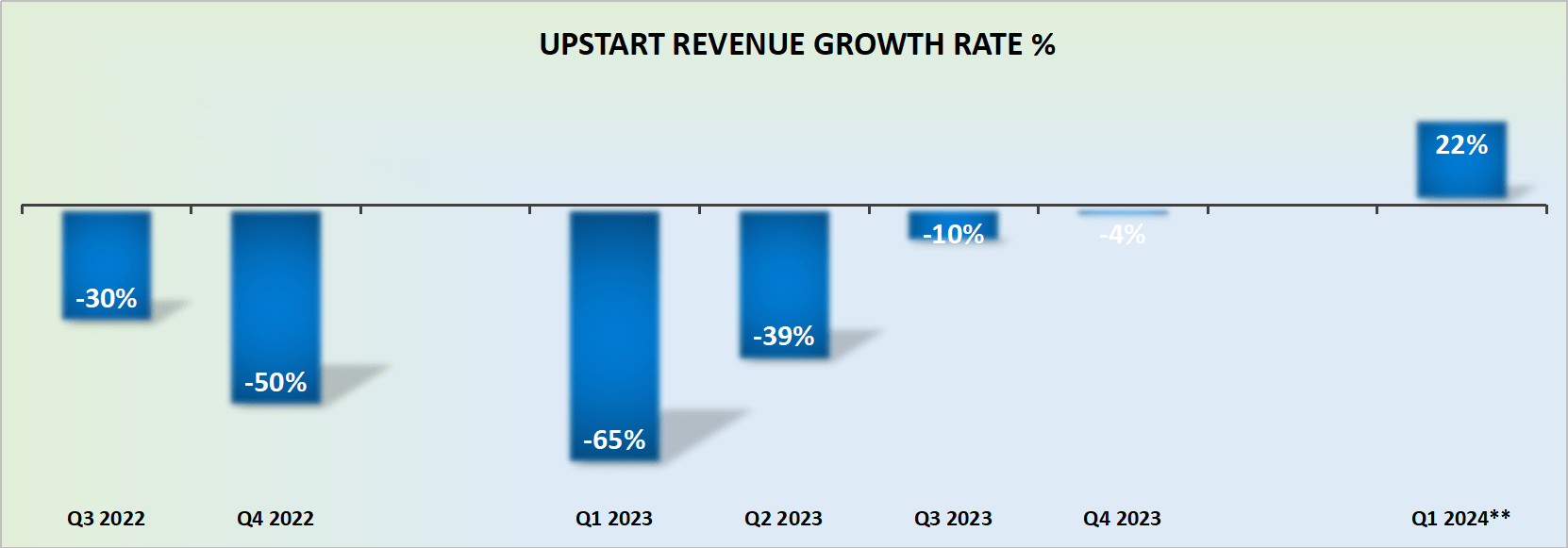

Revenue Growth Rates Should Improve, But Is It Enough?

UPST revenue growth rates

Let me cut to the chase to what I believe is the bull case for Upstart. This business is going to be a smaller and more nimble enterprise.

As Upstart comes up against the very easy comparables of the prior year, particularly in H1 2024, Upstart will have no difficulty in delivering very strong revenue growth rates.

This has been my main assertion for some time with Upstart. But I was wrong. Not wrong on its revenue growth rates, but the question of whether or not Upstart could indeed deliver against its objectives without having to consistently leverage its balance sheet.

And that’s what we discuss next.

UPST Stock Valuation — Too Difficult to Value

For context, consider Upstart’s balance sheet back in Q3 2023.

UPST Q3 2023

What you see is that Upstart held $1 billion of borrowing, while its cash stood at more than $515 million. And Upstart’s management knew that everyone was eagerly watching their earnings results, to see whether they could indeed grow their loan origination business without having to leverage their balance sheet further.

UPST Q3 2024

Another quarter goes by, and Upstart’s balance sheet continues to increase. Admittedly, it’s less than the $1.2 billion in borrowings I stated would cause me to call it a day on Upstart. But at the same time, Upstart is leaking more cash than I had expected.

Furthermore, despite Upstart being under tremendous pressure to carve a path to profitability, Upstart’s guidance for Q1 points to approximately negative $20 million. This is a trifling improvement from the negative $31 million in adjusted EBITDA delivered in Q1 2023.

Consequently, to sum up the picture, there’s more debt on the balance sheet and there’s less cash and Upstart’s underlying cash burn levels are not expected to dramatically improve any time soon.

The Bottom Line

In conclusion, my decision to turn bearish on Upstart Holdings, Inc. has been reinforced by the Q4 2023 results, solidifying my concerns about the company’s trajectory.

Despite the allure of advanced technology and promises of revolutionizing the lending industry, Upstart’s poor profitability profile and escalating debt levels have forced me to reevaluate my optimistic stance.

The consistent rise in Upstart’s balance sheet borrowing, coupled with a diminishing cash reserve, paints a worrisome financial picture.

The company’s guidance for Q1, revealing a projected negative $20 million in adjusted EBITDA, signifies a paltry improvement from the same period a year ago.

As I step to the sidelines, the stark reality of Upstart’s challenges, especially in achieving profitability and managing its debt, underscores the prudent choice to reassess and turn neutral on this stock.