Chip Somodevilla

Co-authored with “Hidden Opportunities”

“They don’t make them like they used to.” I often hear this about the purchased goods, equipment, vehicles, and houses from my grandparents and often from my parents. This expression is often used to convey a sense of nostalgia or admiration for the perceived durability, craftsmanship, or quality of products from the past compared to more contemporary ones. Today, I’m going to discuss this from a human capital perspective.

A study from 2016 revealed that 47% of high school students graduated with grades in the A range. And since then, grades have only gone up. It isn’t just the prices of goods and services that have soared since the pandemic; academic grades have also experienced the steepest inflation ever.

“The average high school GPA increased by 0.19 grade points, from 3.17 in 2010 to 3.36 in 2021, with the greatest grade inflation occurring between 2018 and 2021.” – ACT.org

Grade inflation, as they call it, is worsening and is most prominently seen in higher-income school districts. So, are American students really getting brighter? Sadly, no. Between 1998 and 2016, while the average high school G.P.A. rose, the average SAT scores fell from 1026 to 1002. Among students of the class of 2023, ACT scores were the worst in over three decades.

There’s no shortage of disapproval of the Generation Z population by older members of the workforce. Managers in several industries reveal that Gen Z employees are difficult employees lacking motivation or focus in the workplace. Moreover, Gen Z pursues frequent job-hopping, with the lowest average time spent in a role among all other generations (two years and three months).

Moreover, with remote work, there are increased occurrences of moonlighting (taking up multiple full-time jobs without properly disclosing it to employers and performing the bare minimum on each role) and quiet quitting, severely impacting the workforce’s productivity.

Complaints about the current “young” generation aren’t anything new. Fears for the future aren’t anything new. My parents and grandparents had a lot of negatives to say about my generation. I think we did alright, but I might be biased.

As the world changes, so too will those who take over the companies we invest in and rely on to fund our retirements. Perhaps the scariest thing for retirees to face is that their investments are in the hands of people they can’t control.

As investors, we are direct beneficiaries of stellar strategy through execution and a capable management team can make all the difference for our returns. When we buy a company, we know who is managing it. However, will those who manage our investments in the future be as excellent? We can’t guarantee that.

It’s that unknown that led Warren Buffett to famously state:

“I try to invest in businesses that are so wonderful that an idiot can run them. Because sooner or later, one will.” – Warren Buffett

Let us look at two picks from asset-heavy industries that provide critical services to the population with terrific pricing power to help “idiot-proof” our income and retirement. Let’s dive in!

Pick #1 UTF – Yield 8.8%

There are lingering doubts about the state of the economy – will we achieve a hard landing, a soft landing, or no landing at all? But no matter the outcome, we should invest in a manner that allows our income to thrive.

The U.S. continues down three notable paths

-

Low-carbon energy systems

-

Expand domestic manufacturing

-

Larger data centers for energy-intensive artificial intelligence needs

These initiatives have solid backing from the Federal government through three notable programs – the IIJA (Infrastructure Investment and Jobs Act), the IRA (Inflation Reduction Act), and the CHIPS (Creating Helpful Incentives to Produce Semiconductors) Act. Billions in federal and state government funding will flow into several companies’ top lines, ensuring robust profitability as high material costs fade.

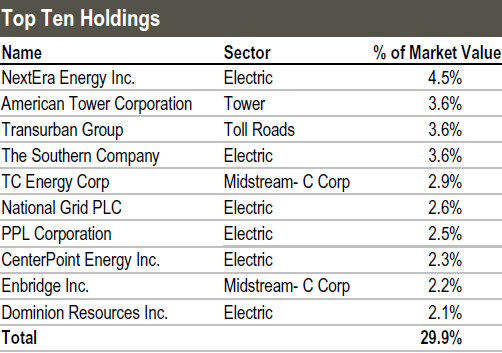

We like this defensive sector and seek to improve the reliability of our income through diversified exposure to this lucrative yet deeply discounted sector. Cohen & Steers Infrastructure Fund (UTF) is a highly diversified fund with its assets invested across 248 companies. The company’s top 10 positions are some of the largest electric utility, midstream, and roadway companies, constituting about ~30% of the asset value. The extensive diversification provides an excellent cushion for the fund to ensure distribution safety from the trio of federal programs. Source

UTF Fact Sheet

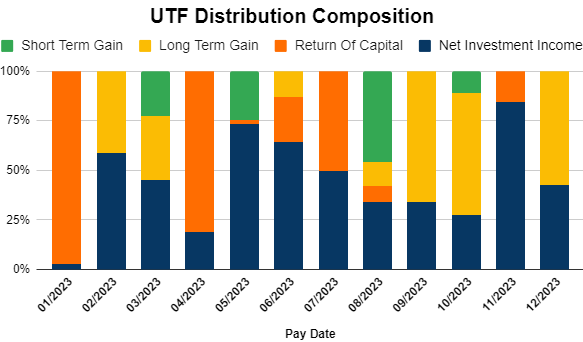

UTF operates with a 30% leverage, with 85% carrying a fixed weighted average interest rate of 1.8% and a duration of three years. The fund distributes $0.155/month, an 8.8% annualized yield, and this distribution is fueled through a combination of net investment income, capital gains, and some return of capital.

Author’s Calculations

It must be noted that UTF reported almost $545 million in unrealized asset appreciation on its semi-annual report from June 20, 2023. This is adequate to fuel the shareholder distributions for more than three years.

As America continues to build a modern power grid with an increased mix of renewables and natural gas, bringing manufacturing jobs home, and improving our roadways and railways, you can collect your share from UTF’s monthly distributions. The CEF trades at a modest 2% discount to NAV, making it a bargain to lock in high yields from a defensive sector that’s well positioned to see substantial cash infusion in the years ahead.

Pick #2: Antero Midstream – Yield 7.4%

Global macros point to energy prices to remain volatile in 2024. But midstream’s defensive contracts, fee-based operating structure, and contractual protections to pass through inflation pressures make them uniquely positioned to benefit compared to other energy market segments.

Antero Midstream Corporation (AM) owns a vast portfolio of transportation, storage, and processing infrastructure for natural gas and LPG (Liquid Petroleum Gas) exports to international markets. Notably, at least one-third of AM’s LPG production is delivered to developing nations, where it’s a critical fuel source. AM mainly provides Antero Resources (AR) gathering and processing services under long-term fixed-fee service agreements.

AM also is a key player in providing a closed-loop system of freshwater pipelines and storage facilities, delivering water directly to pad sites, improving the efficacy and cost effectiveness of operations while being a greener option vs. trucks.

Note: AM is structured as a C-corp, so unlike many peers, it issues a 1099 at tax time.

AM is one of the few firms that uses the term “Free Cash Flow After Dividends” to indicate excess profitability available for value-enhancement opportunities. During Q3, AM generated a record $251 million of adjusted EBITDA (a 12% YoY growth) and $30 million in free cash flow after dividends. The company utilized this FCF toward debt reduction, extinguishing $106 million in debt year-to-date and bringing down the net leverage to 3.4x (from 3.7x at the end of FY 2022).

For FY 2023, management has provided guidance of adjusted EBITDA between $970-990 million and FCF of $565-585 million. This places the annual dividend at a 43.8% EBITDA payout and 74.8% FCF payout ratio, respectively. AM pays a quarterly dividend of $0.23/share, a 7.3% annualized yield. There are no reasonable expectations of dividend raises at this time, but we see the dividend getting increasingly safer through profitability growth.

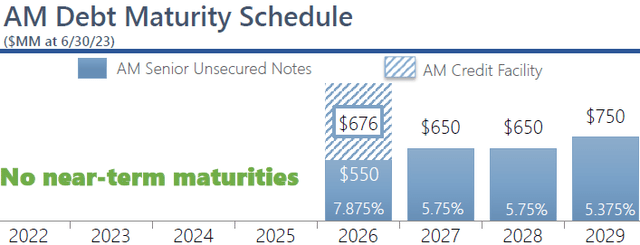

AM has no near-term debt maturities until 2026, and the company is actively paying down debt to reduce interest expenses. Notably, the company spent 16.7% less YoY toward interest expenses in the nine months of FY 2023, an impressive figure at a time when companies across the board are facing soaring borrowing costs amidst high interest costs. Source

November Investor Presentation

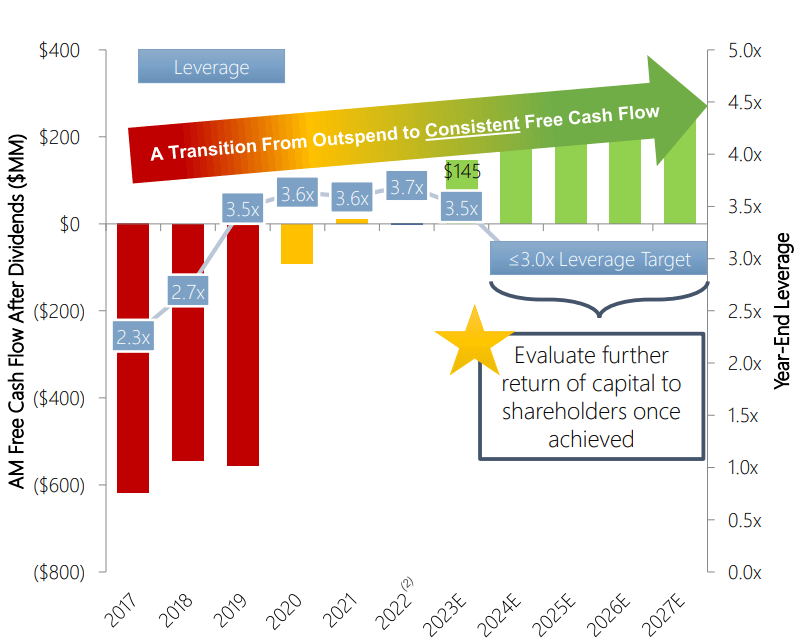

Reducing interest expenses further strengthens the dividend safety by adding to the FCF after dividends. AM is on track to reach its 3x leverage target by 2024, and management projects $1- 1.3 billion in cumulative FCF after dividends through 2027. Source

November Investor Presentation

During the Q3 conference call, AM CFO dropped hints of shareholder value creation pursuits through share repurchases and further debt reduction with the excess FCF after reaching the debt targets.

There are numerous findings about the critical deficiencies in storage and transportation infrastructure in the United States that ensure a resilient system of natural gas supply across the country. As U.S. natural gas exports hit record-high levels, the requirement for infrastructure expansion intensifies. With robust asset utilization, continued FCF growth, debt shrinkage, and a reliable 7.4% yield, AM stands out as a compelling cash flow powerhouse for your income portfolio.

Conclusion

As the years go by, things change. One of the major changes will be the management teams we invest in today will retire and be replaced. Will the new management be “good”, “great”, or “bad?” We won’t know until we see what they do. And this, all the more makes the case for current income as we take our returns today and redeploy as we see fit.

We employ several techniques to safeguard our financial future from shocks in the form of unfavorable strategic changes that negatively impact our income, or from incompetent management that cannot execute to meet our income needs. We choose securities with regulatory requirements to pay dividends or from traditionally dividend-focused industries. Moreover, we employ safety through diversification by spreading our investments across 45-plus instruments, so that bad news from a few doesn’t have a material effect on our portfolio or its income-generation potential.

No matter how the workforce evolves, I know people will heat and cool their homes, pay tolls on their commute, enjoy BBQs in their backyard, and increasingly use the Internet. I want to collect some fees from all these activities, so I invest in simple but critical businesses with well-established operations and terrific pricing power. I’m establishing my financial freedom not just from the need to work or irrational market conditions, but also from the risk of bad leaders in corporate America. “They don’t work like they used to.” – Are you prepared?