Debt has long been a dirty word in law firm circles. The idea of relying on bank loans to fund a legal partnership feels both low-grade and risky.

But law firms are outliers in the business world. Most large institutions see debt as an important tool to helping them achieve their aims. Apple, one of the world’s largest companies, has around $100 billion of debt.

According to data from Law.com Compass, only 38% of AmLaw 200 law firms have any debt. This jumps to 65% among U.K. Top 50 firms, but that number has been falling and still remains low compared with listed corporations.

You can get a feel for how comfortable firms feel about the concept by how open they are about it. The topic is like a secret among law firm leaders, only revealed in vague terms or via historic account filings.

Freshfields Bruckhaus Deringer is one of the world’s oldest legal institutions and I’d wager it has never held any debt before now. Even insiders don’t seem to know for sure, but the firm’s historic limited liability partnership accounts—which go back to 2009—certainly indicate this.

So why have the firm’s latest accounts, as of April 2023, suddenly shown debts of nearly £90 million?

I propose one obvious reason, one less obvious one and one foreboding long-term problem.

The obvious reason is the changes to the U.K.’s tax rules this year, which mean many firms are faced with the prospect of paying two years’ tax in one go.

According to law firm financing experts, this is affecting a wide variety of U.K.-based law firms and has caused many to take on debt to fund the payment. It is too soon to know which firms have done this but, based on analysis last year, firms including Womble Bond Dickinson, Stephenson Harwood, and Watson Farley & Williams had relatively low cash balances compared with their peers and may have chosen to take on more debt.

But as of April 2022, Freshfields had a healthy cash balance and zero debt. Over the course of the next 12 months the firm’s cash position almost halved to £58.7 million and it took on its £88.3 million of bank loans and overdraft.

This period coincided with its continued aggressive expansion efforts in America, which could be the less obvious reason for its balance sheet change.

Taking on debt to fund such expansions is a way of spreading the cost across future generations. Instead of calling on partners to stump up more capital or suffering a big drop in profits per equity partner, using loans that will be repaid over a longer period makes sense. Why should this generation of partners have to foot the entire bill of an expensive long-term investment?

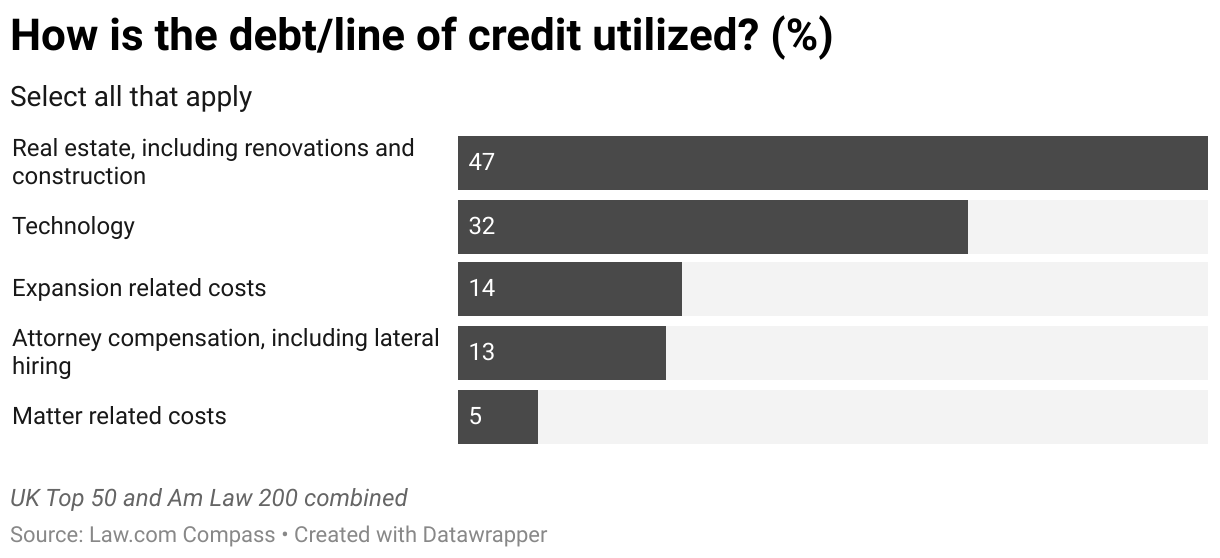

Data from Law.com Compass shows it is usually investment for the long term that causes firms to borrow.

But this is where expansion efforts get tricky. There is always a slight fear that too much debt could bring a firm down. Who wants to sign up to or stay in a partnership that has to constantly pay money off? Once enough people leave, others start to lose confidence in the stability of the firm. A common trait among firms that collapse is that they held debt.

The key question is whether the debt amount is serviceable. How does it compare with revenue and profits? In Freshfields’ case its revenue is close to £2 billion, which makes £88 million look pretty trivial. Most importantly, how does it compare with invoiced work and unbilled time?

And yet simply being able to service debt is not the end of the story. Expansion efforts and planned investments are rarely financed via debt alone. A more sensible strategy is to build up cash reserves over several years to help fund strategic investments.

And this leads onto the longer-term, foreboding problem: that firms taking on debt may be doing so because they are struggling to keep up with the market.

Think back to the fact that U.S.-based firms are more likely to be debt free. This is not just about of U.S. firms operating in a bigger, more lucrative economy. According to senior executives at Citi, U.S. firms’ financial management has been more conservative over the last decade.

In 2012, they explain the top U.K. firms were typically capitalized at a higher level than those in the U.S. A decade later, it is the other way around.

Michael McKenney, a managing director in Citi Global Wealth at Work’s law firm group, says this is because U.S. firms have gradually increased individual partners’ capital requirements to enter the equity. On average at large firms this now stands at $600,000. In comparison, U.K. firms haven’t changed their requirements and on average theirs stands at $450,000.

Unsurprisingly, the U.S. firms have built up bigger cash balances as a result, which offers them a cushion to secure expensive lateral partner hires, sign up to new offices, buy in the latest technology and even agree mergers.

In this context, firms’ willingness to take on debt now offers an insight into their management decisions over the last decade or so.

No wonder they want to keep their debt levels a secret. Not only does it shine a light on their financial position right now, but it also exposes their long-term financial planning, or lack thereof.