Igor Kutyaev

Markets are hitting key inflection points across multiple asset classes heading into the Fed meeting on Wednesday. The dollar, rates, commodities, and equities are all at critical technical levels, suggesting the market is waiting to hear what the Fed says.

It could be a sign that the next move the market makes will have a longer-lasting impact, similar to what triggered the easing of financial conditions at the beginning of November when this current equity market rally started and allowed financial conditions to ease.

Rates

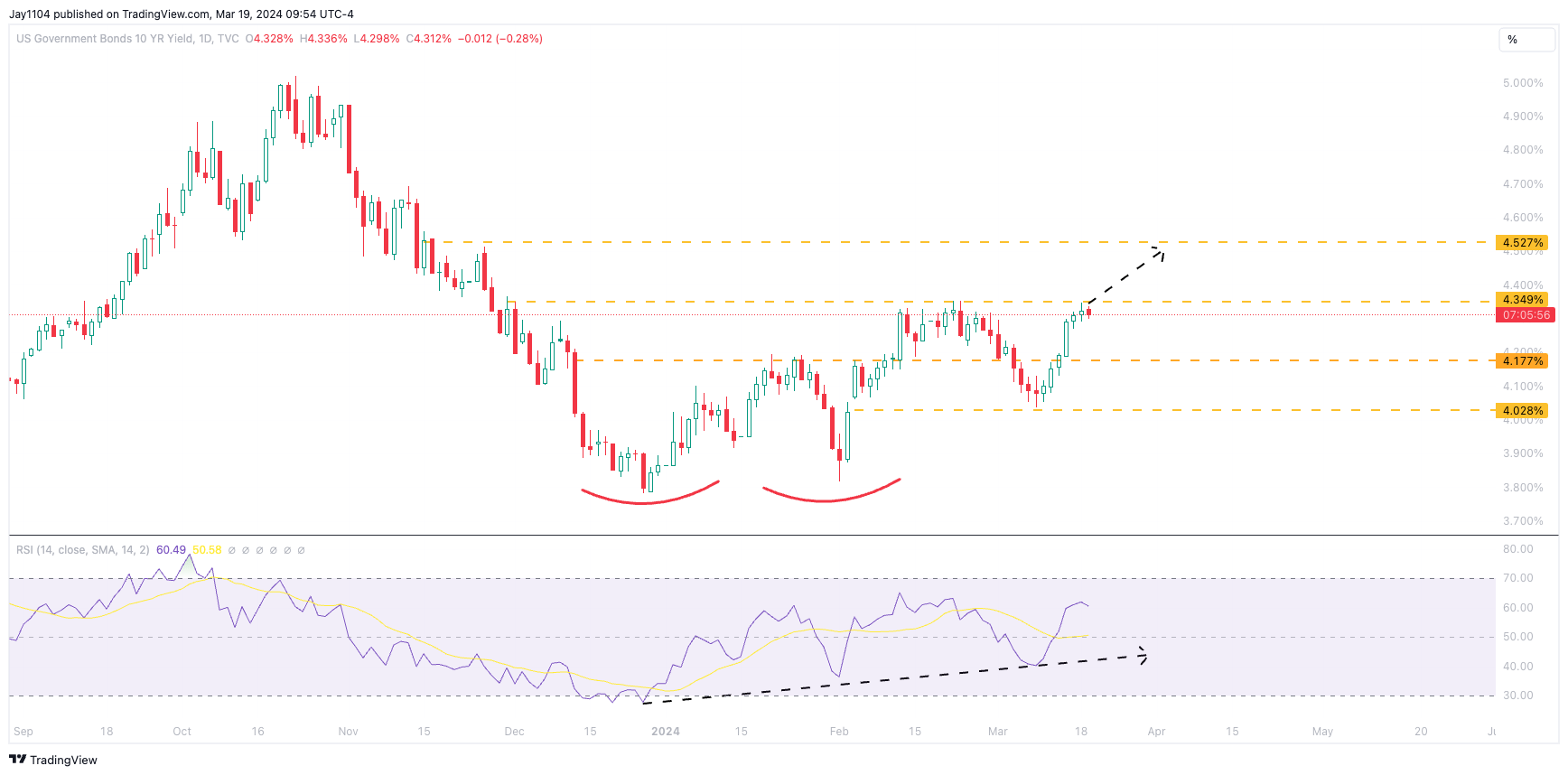

Right now, the most apparent inflection point comes in rates and in the 10-year Treasury, which is currently at a resistance level of 4.35%. The 10-year yield has been testing this level since Feb. 13, following the release of the January CPI report. The 10-year is now making a second pass at this resistance level. A breakout in the 10-year above 4.35 could result in the 10-year rate rising to around 4.5%. Meanwhile, if the 10-year rate should fail to break out on a more dovish Fed take, we could see the 10-year drop back to 4%.

Trading View

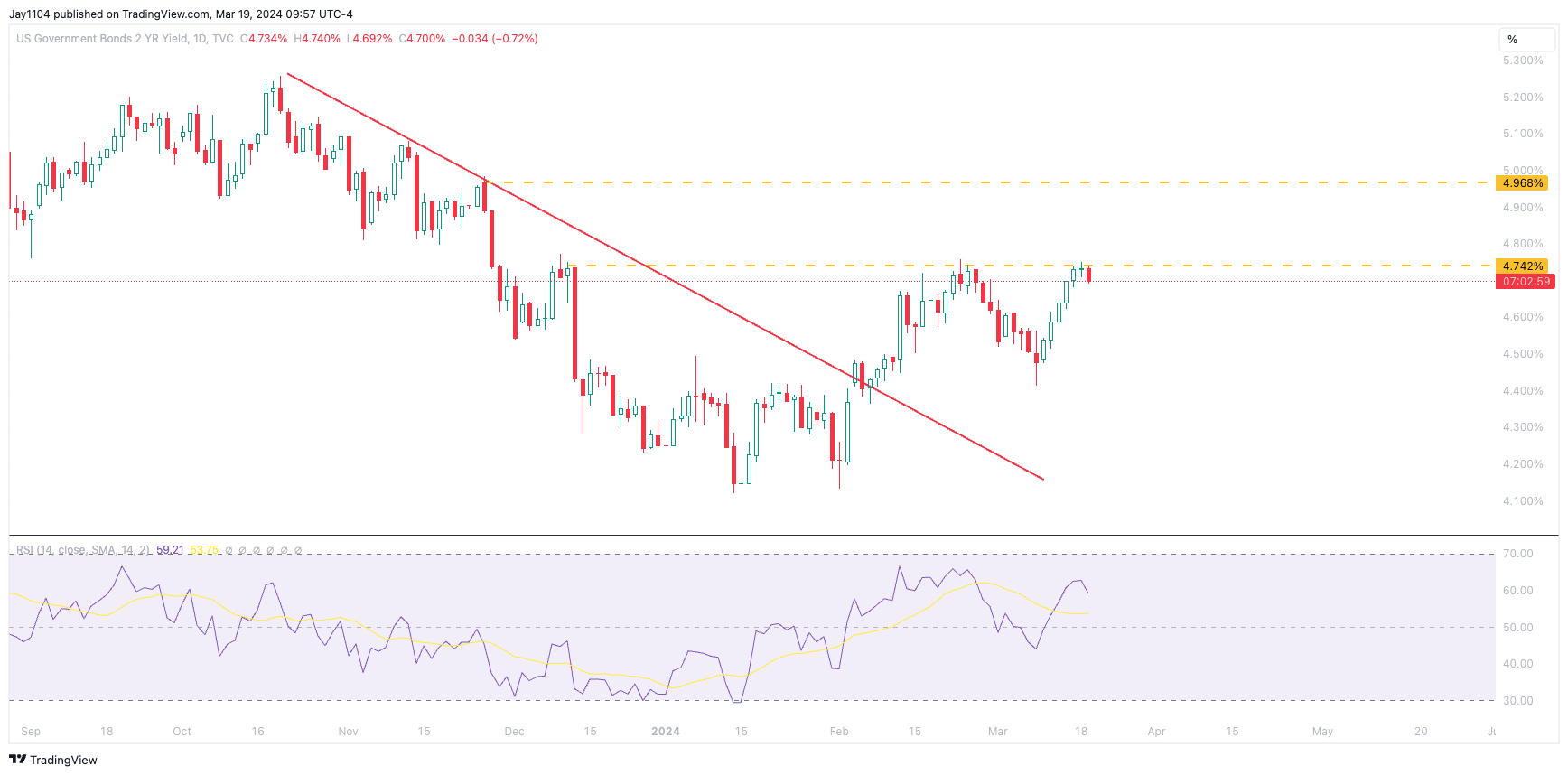

The 2-year yield has struggled to push above 4.75% in the last few days. Like the 10-year, the 2-year rose sharply in mid February following the hot CPI report. But more importantly, the 2-year is testing resistance for a second time. It will take a more hawkish than expected Fed to get the 2-year to break out, but if the Fed should dial back on rate cuts, the 2-year could be heading back to the 5% region. A failure to push beyond 4.75% likely leads to the 2-year dropping back to 4.5%

Trading View

FX

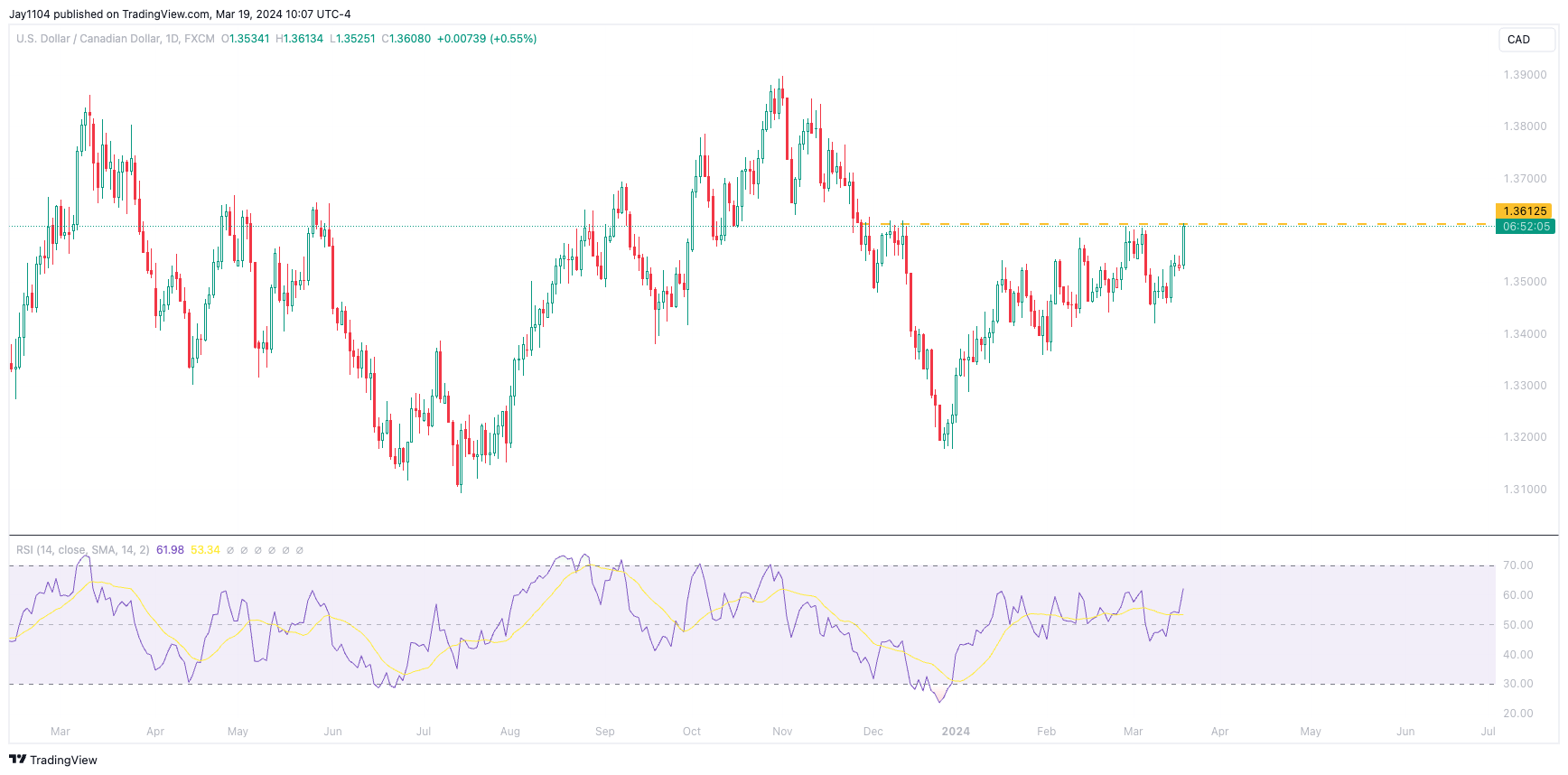

The dollar and some of its currency pairs, especially against the Canadian dollar. The US dollar has been strengthening against the Canadian dollar in recent weeks but has been unable to break through the 1.36 resistance area since the beginning of December. A move above the 1.36 resistance level likely sets up a move to higher levels and potentially back to the highs around 1.39, a sign of the US dollar strengthening. Meanwhile, a failure to push beyond 1.36 likely leads to a drop back to 1.345.

Trading View

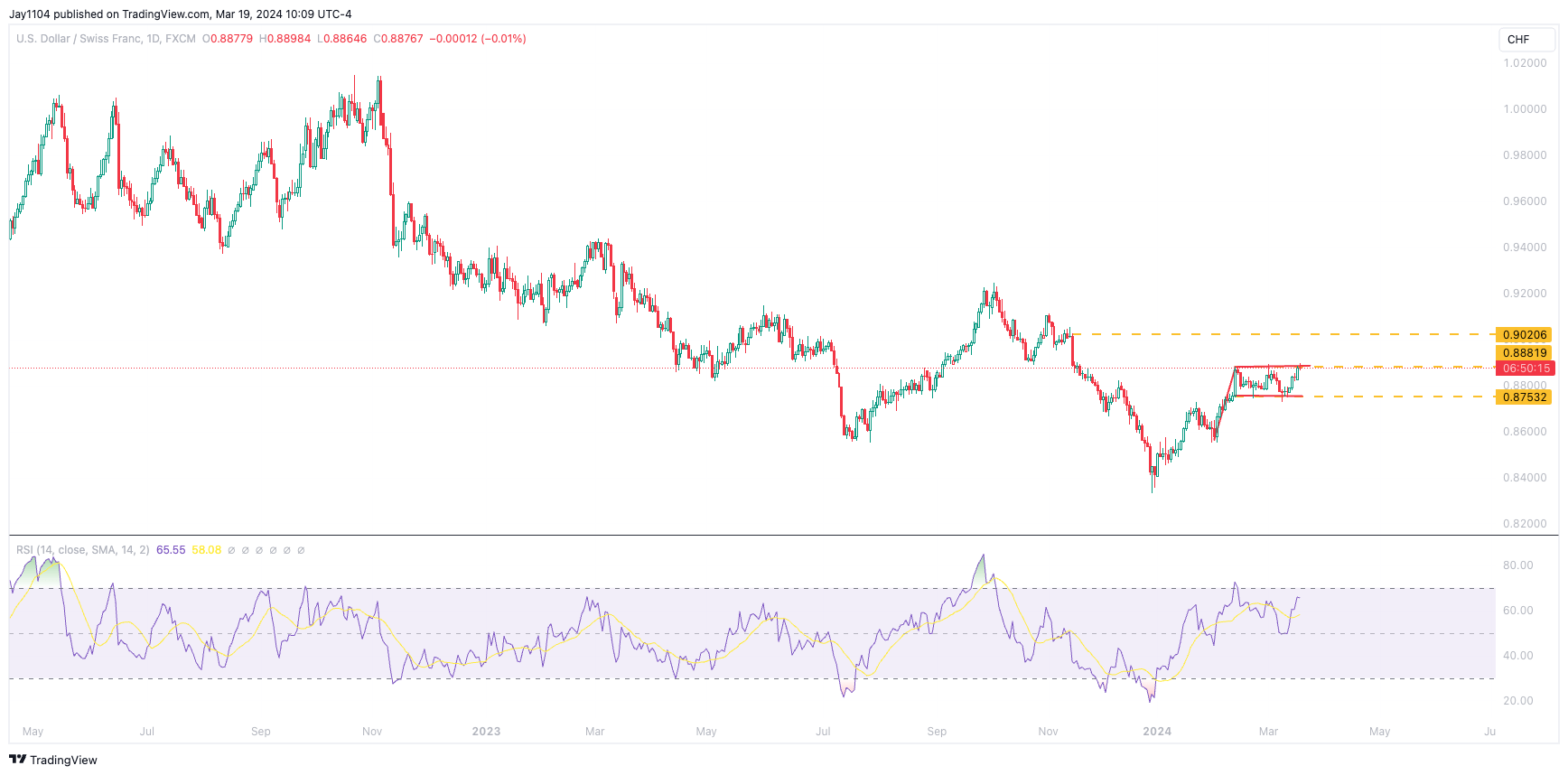

The same is true for the US dollar vs. the Swiss Franc, with the dollar struggling to get above and beyond resistance at 0.89. A move above 0.89 would again be a sign of dollar strength and could potentially lead to a move higher against the franc to around 0.90. Meanwhile, a failure to push higher probably leads to a drop to the lower end of the range around 0.87.

Trading View

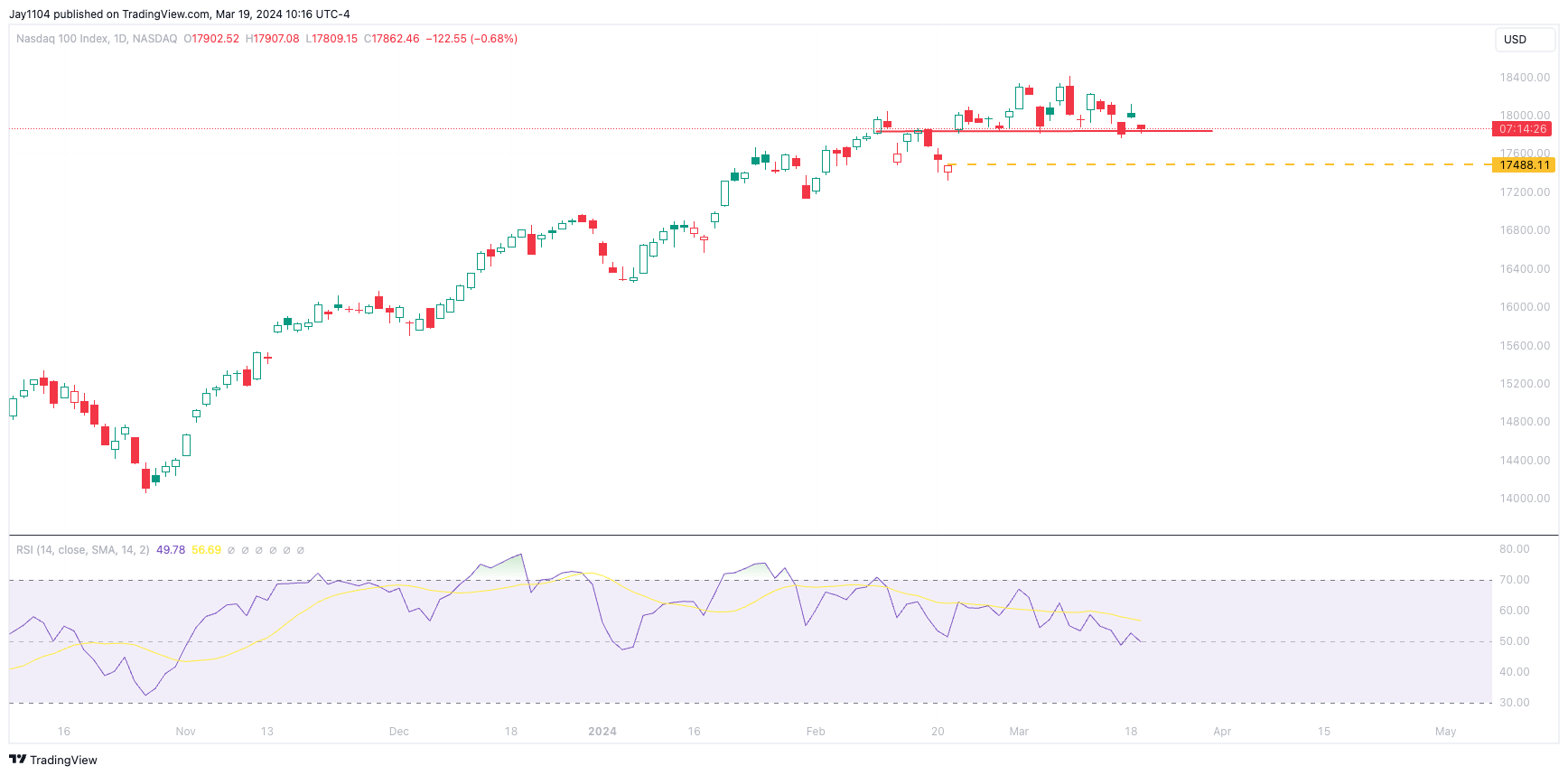

Nasdaq

The Nasdaq 100 has consolidated sideways since Feb. 9, right around the same time as that January CPI report. Now, the Nasdaq 100 is sitting on support at 17,850, with a break of support setting up an initial decline to around 17,450, which fills a gap from Feb. 22, following the Nvidia post-earnings rally. However, if the Nasdaq should hold support and bounce, it could result in the Nasdaq rising back to the highs around 18,300.

Trading View

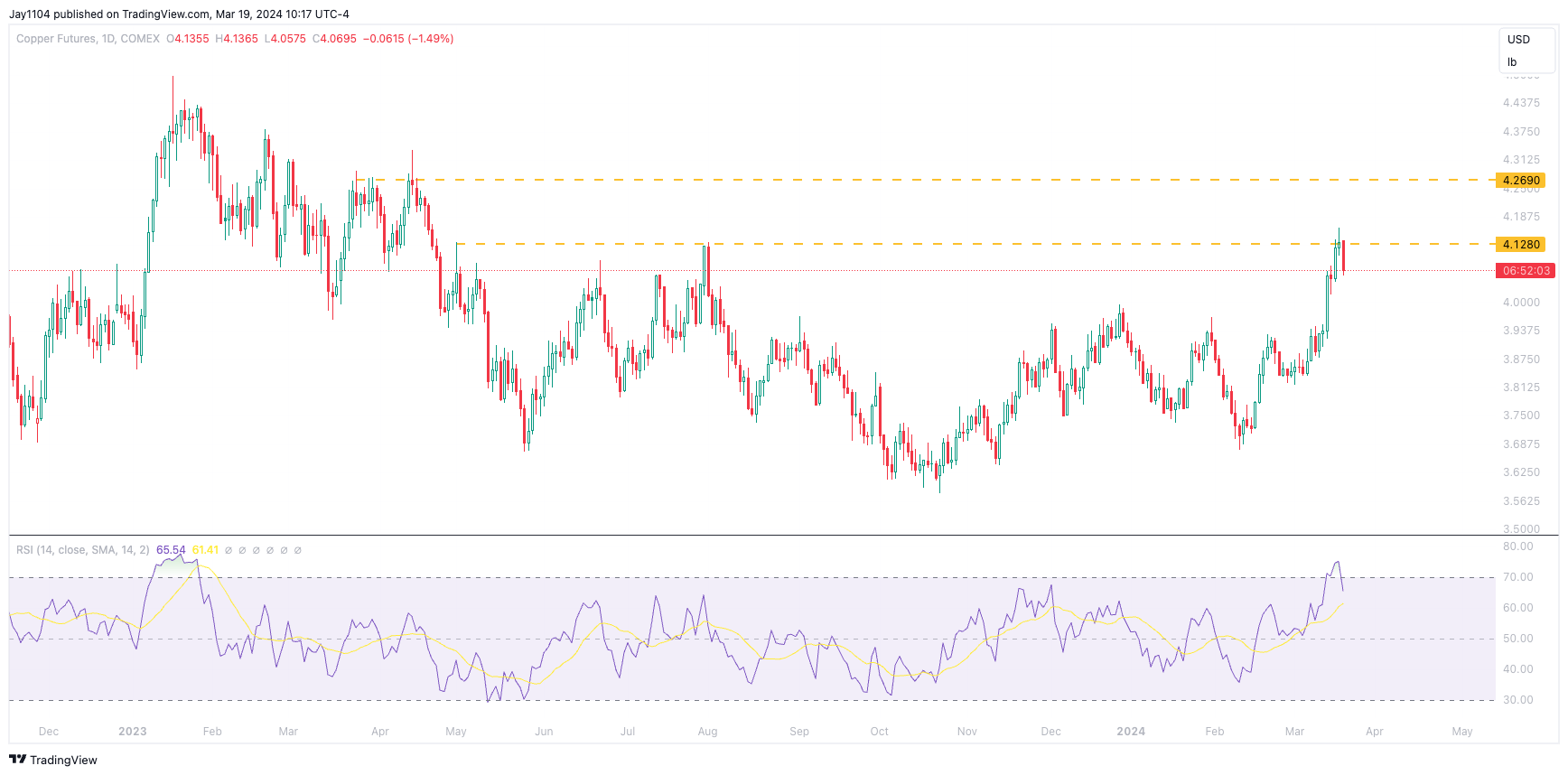

Copper

The same thing is visible in copper prices, which have rallied to a resistance at the $4.13 level, which breaks out potentially sending copper to around $4.26, while a failure to advance could send the copper lower and back below $4.

Trading View

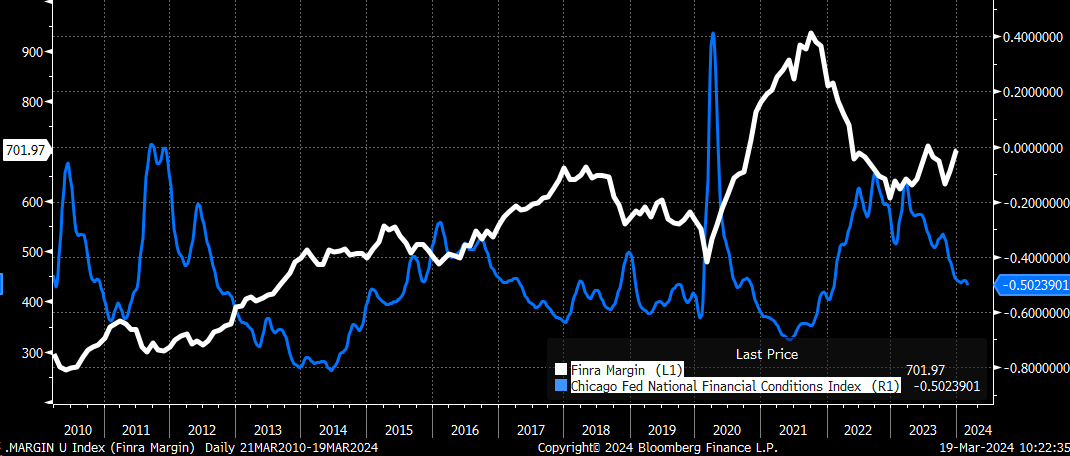

Financial Conditions

The key here is how the market is waiting to get the go-ahead to either tighten or ease financial conditions. Rising rates and a strong dollar would result in tightening financial conditions, which would be bearish for equity prices. However, a dovish Fed would likely result in rates and the dollar falling, easing financial conditions and allowing equities to rally.

While it may seem as if the stock market doesn’t care or that liquidity is all that matters, that’s not the case. The stock market is getting its lead from rates and the dollar and, more importantly, their impacts on financial conditions. When financial conditions are tightened, liquidity is pulled back on, and when financial conditions ease, liquidity is added to the system.

When comparing FINRA Margin balances versus the Chicago Fed Financial Conditions index, it’s fairly easy to see the inverse relationship the two have had over the past decade or so. The easing of conditions since March 2023 has allowed leverage to enter the market, while the tightening of conditions between May 2021 and October 2022 led to the removal of leverage.

Bloomberg / FINRA

So what the Fed does and says tomorrow will impact whether stocks, rates, and the dollar rise or fall, and the impact of that direction will directly impact financial conditions and, in effect, carry out Fed monetary policy, whether it is the Fed intent or not.